Let’s get right down to it: Shopping for a home is fun. But once you find the home that makes you swoon, things start to get real—real fast.

Think of making an offer on a home as setting the roller coaster in motion: You might have sharp drops in emotion and slow, trudging climbs to success, but the ride won’t end until the car slows down and the safety bar is lifted. (OK, this metaphor is now officially over.)

But to begin the process, you need to know how to make the right offer, an offer that will end with your receiving the keys to your new house. So check out some of these agent-approved negotiation tactics to make the offer process a whole lot less bumpy.

Pick the right price

Just because a home is listed for $400,000, it doesn’t mean the home is actually worth that much.

It all depends on the current conditions of the local market. If you’re buying in a hot market—especially places with low inventories—offering substantially below asking price is “probably wasting your time,” says Mindy Jensen, a Realtor® with Equity Colorado. But if a home has been sitting unsold for a few months, the sellers may not expect full price. Your best bet at measuring prices in your target area are comps, or what similarly sized homes nearby have sold for recently.

Work with your real estate agent to determine a fair offer. They will have the best read on pricing and marketplace dynamics, and can walk through the local comps with you. Your agent can also help you determine what a fair discount might be without offending the seller. While specific numbers will depend on your market, a rule of thumb is that it is unrealistic to go below 5% of a home’s list price unless it’s been sitting on the market for months. Which leads us to…

Lowball with care

Sometimes a home is priced just too high—no ifs, ands, or buts—or perhaps it’s been sitting unsold for half a year. In those situations, a lowball offer well under asking price might be the right strategy to get the home you love for a bargain price. However, this is a tool to be deployed rarely and with great care—especially if the current owners have lived there for many years.

“Longtime owners usually have tons of pride in their home, and want the new owners to love it like they do,” says Jodie Burns, a Realtor with McEnearney Associates. “Buyers who lowball run a risk of angering the seller and losing the house. Ideally, you’re looking for a closing where both sides feel like they got a fair deal.”

So don’t lowball unless both you and your agent agree that it’s the best tactic to sway a seller. It can be perilous, so it’s best to keep this strategy on the sidelines unless you’re fairly certain it won’t cause a seller to walk away entirely.

Also, think about the big picture. Don’t let a (relatively) small amount come between you and a house you adore. “If a couple of thousand dollars is going to keep them out of a home they love, I remind buyers how little that amount translates into a monthly payment,” Burns says.

Consider contingencies

Along with the price, you’ll also want to factor contingencies into your contract. The more hurdles in the way of the sale, the more likely one of them will trip you up.

For example, do you need to sell your own home first, which requires a selling contingency? Work with your agent to decide what you’ll ask for off the bat—and consider dropping some requests if the market is hot.

As Jensen explains, “Your chances are best if you ask for the fewest things.”

That said, don’t put yourself at risk to get the home you love. Some aggressive buyers might advocate dropping the home inspection clause to sweeten an offer, but that can be dangerous, especially in older homes.

Keep your emotions in check

Yes, the search seems to have dragged on forever; yes, this home has everything you need. But keep your wits about you.

“Don’t fall in love,” Jensen says. “Falling in head over heels with a home can make you do ridiculous things, like overpay.”

Plus sometimes, even an “excellent offer may not be accepted,” says Vici Boguess, a Realtor with the Burke Boguess Zimmerman Group in Alexandria, VA. Don’t assume a rejection is an insult—the sellers might just dislike some of your contingencies or are holding out for a better offer. So, don’t assume it’s over until it’s over.

The right professional help, asking price and coat of paint can make selling your house easier.

You may be one of the many homeowners considering a home sale to potentially benefit from the seller’s market that exists throughout much of the U.S., where buyers outnumber available properties, leading to higher prices and plenty of bidding wars.

But selling a house can become more difficult if you ignore the tried-and-true practices that have helped home sellers in the past. “It’s a hot market, but it’s a hot market for things that are priced correctly and prepared to come to the market,” says Molly Gallagher, real estate agent and partner of the Falk Ruvin Gallagher Team, part of real estate brokerage Keller Williams Milwaukee North Shore in Wisconsin.

Here are 12 mistakes to avoid when selling your home:

Working alone.

Waiting for the home selling season.

Pricing too high.

Refusing to make changes.

Keeping clutter.

Opting not to neutralize.

Skipping major repairs.

Cutting costs on photography.

Hiding problems.

Being unavailable.

Being unwilling to negotiate.

Letting your emotions get the best of you.

Working Alone

Not hiring a real estate agent to represent you may seem like an easy way to avoid paying commission, but you’ll miss out on a real estate agent’s market knowledge, contacts and help with the process. Unless you have a real estate license or are planning to find an iBuyer, a real estate agent is key to a successful – and less stressful – home sale.

For-sale-by-owner properties tend to sell for a lower price overall. In the National Association of Realtors’ 2020 Profile of Home Buyers and Sellers released in November 2020, FSBO homes sold at a median of $217,900, compared to a median sale price of $242,300 for properties that sold with the assistance of an agent. If you’re looking to sell your home for its full market value, professional insight is more likely to get you there.

Waiting to Sell

Spring and early fall are often hailed as the best times to sell a house, but that doesn’t mean you should wait months to put your home on the market. While December and August see the fewest sales homes still sell every month of the year, says Anne DuBray, a real estate broker with Coldwell Banker Realty in Deerfield, Illinois.

In fact, February is the best month to put your property on the market, DuBray says – even in places that see long, cold winters like Chicago and Milwaukee. “People are less distracted in that month than every other month of the year,” DuBray says.

Pricing Too High

You want to sell your house for top dollar, but be realistic about the value of the property and how buyers will see it. If you’ve overpriced your home, chances are you’ll eventually need to lower the number, but the peak period of activity that a new listing experiences is already gone.

“Time will kill you,” DuBray says. “You still think you’re going to get showings and showings (as time goes on) and you just don’t.” For that reason, it’s important that your real estate agent is honest with you about what your home will sell for, based on the recent sales of similar homes in the area.

Refusing to Make Changes

Unless you’re planning to sell your house to an investor who will flip the property, selling your house “as is” won’t yield the highest possible sale price.

Homebuyers today expect move-in ready conditions and want to see a blank slate that allows them to picture themselves living in the home. That means you’ll need to update appliances, paint walls neutral colors such as gray or khaki and remove old carpeting.

Keeping Clutter

It’s tough to remove belongings while you’re still living in your house, but presenting each room and space in its best light means you’ll need to declutter in more ways than one. Get rid of items you don’t need anymore, but also remove oversized couches and other large furniture that dwarfs the room, clear out closets so they don’t look overcrowded and put away decor that displays too much personal detail.

“Just because you see any empty surface doesn’t mean you have to have something there. Give the eyes a moment to rest,” wrote Jessica Harris, an interior designer and manager of production design at furniture retailer Living Spaces, based in Southern California, in an email.

Opting Not to Neutralize

While removing personal decor choices is a part of decluttering, it’s also an important part of neutralizing your house so the buyer doesn’t immediately think of the people who currently live in the home.

“Remember to remove personal photos, memorable items and more from the home,” Harris says. “You want the potential buyers to envision it’s their home, not yours. If it’s something you question, go with your gut. Think simple, clean and refresh.”

That goes for your personal design tastes as well. Busy wallpaper, bright colors and trendy furniture can look amazing in your home, but buyers won’t be able to look past them and consider the space first.

Skipping Major Repairs

Pulling up carpeting and painting the walls are relatively easy tasks to tackle, but you’ll want to fix major issues as well. Cracks in the foundation or a new roof are expensive fixes that you may be wary of taking on, especially when you won’t likely recoup the entire cost in the sale. But you’re better off fixing these issues now rather than having the buyer ask for a credit to cover the cost of the repair later. This way, you have more say over who does the job and the total cost of the repair.

Plus, newly replaced features become a selling point once the property is listed. Gallagher says replacing the roof before listing your home can be cheaper than the cost a buyer would subtract from an offer. “You’re likely to get that (cost back) in the sale price if you do the new roof,” Gallagher says.

Cutting Costs on Photography

The first way many buyers see your property is by viewing photos of the house online, so don’t make them cross your house off their list before they’ve even visited.

Most real estate agents include professional photography in their marketing budget. Even if you can’t get a professional, make sure all photos give the buyer an idea of the size of the rooms. Also make sure photos are well-lit and keep you out of the frame in any reflections.

Hiding Problems

If there are problems with the property you can’t afford to repair before putting it on the market, you have to be honest about them – even if they’re not visible to the naked eye. Sellers are required to note recent repairs, problems and updates in the seller’s disclosure.

“All those things are going to come up in the inspection,” Gallagher says, adding that it’s best for everyone to know in advance rather than let the buyer have second thoughts after reading the inspection report. Even if the inspection doesn’t catch a leak or structural issue, but the buyer can prove your knowledge of it later, you could be facing a lawsuit.

Being Unavailable

When your house is on the market, showing the house should be your priority. That means if you get a call that a buyer would like to tour the house, you need to be able to leave the house in pristine condition quickly.

Even on holidays, an interested buyer is likely serious about making an offer and you shouldn’t refuse a showing. So while you’re trying to sell your house, aim to hold Thanksgiving or other holiday celebrations elsewhere.

Being Unwilling to Negotiate

If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate. While you’ll naturally feel your asking price is more than fair, the only way to come to a successful deal is to make sure the buyer also feels like he or she benefits.

If you would like to see the sale price come up, consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.

Letting Your Emotions Get the Best of You

It’s natural to have some emotional attachment to your house after living in it for years and celebrating milestones, holidays and accomplishments with your family and friends there. But you have to view selling your house as a business deal. A low offer is not a personal affront, but a start that can either be negotiated up or declined. Plans to renovate part of you house are not an insult to your taste, but a difference in preferences.

The more you can approach the sale of your house as a business deal, the better off you’ll be to make the transaction as smooth as possible.

East Turlock… Single-Story Home on a Cul-de-Sac Lot!!! This Semi-Custom Home is Approx. 1626sf with 3 Bedrooms and an Office. High-Vaulted Ceilings in the Large Family Area. Large Sunroom to Entertain or Put your Game Room. Updated Kitchen with Granite Counters. Big Master Suite with Walk-in Closet, Tub, Shower Stall, and Outside Access. Backyard has an insulated Shed for Storage or a Crafts Room. Lots of Fruit Trees. A Very Nice Family Plan!! A Must See.

n average, employees who get a job offer that requires them to relocate have a mere 2 weeks to decide whether they want to formally accept the position. The timeline could be even shorter in hot job markets—employers are wary about candidates shopping their offers around to competitors for a better setup…so they turn up the pressure.Regardless, 14 days or less isn’t much time to think over such a big change. In addition to making a career shift, a job transfer means finding a new house, general physician, grocery store, and social circle. And as a homeowner, you can’t just break your lease and be on your way—you’ll have to sell the house (likely on a tight deadline).Whether you’re the type of person who makes pros and cons lists or just needs to talk things through, we’ve rounded up 10 critical job relocation questions to ask before you sell your house to uproot for work so you cover all your bases.

1. What are the financial implications of selling my house and buying one in a new location?

Before you make the decision to relocate, it’s a good idea to ballpark how much you’d pocket from selling your house, and figure out how far that money would stretch in a new location that may have a drastically different cost of living. Will you be going from a spacious single-family to a shack with shared walls in a more expensive city? Or could a relocation mean you’re finally able to trade up to a nicer place?

Don’t just guess… do the math. You can follow this quick step-by-step:

Find out the value of your home

Get your estimates

(Note that online home valuation tools can give you a decent home value average, but you should consult a top local real estate agent who can conduct a formal comparative market analysis before setting your list price.)

Ballpark your home sale proceeds.

Once you have an estimate for what your house would fetch on the market, subtract your outstanding mortgage payoff amount and the estimated costs of selling a house including agent commissions (5%-6% of the sale price), transfer fees, and home preparations and repairs—likely amounting to 7%-12% of your home’s value depending on its condition.

Calculating how far your new salary will cover your new cost of living is key to deciding on the size of your new home and your price range. “That’s one of the questions you want to answer: What kind of lifestyle changes are you going to be experiencing in reference to cost of living?” said Gene Darden, a Relocation Specialist.

For instance, Darden explains: a 4,000-square-foot house in the Birmingham, Alabama, market costs about $500,000…In Atlanta, the same size costs twice as much.

There are lots of cost of living calculators online to help you evaluate how far your dollars will stretch. Sperling’s Best Places, the company that provides statistical information on crime rates, climate, and other factors, provides a cost of living comparison that includes housing, food, utilities, transportation, health costs, and taxes.

Want to dig deeper? Bankrate’s Cost of Living Calculator starts with a salary comparison between cities, then itemizes for costs such as specific foods (ground beef, coffee, half-gallon of milk), gasoline, clothing items, services (dry cleaning, hair salon), clothing, and toiletries such as ibuprofen and toothpaste.

Based on your home sale proceeds estimate and new monthly salary, you can figure out how much house you can afford in your new city.

“If they come to me and say, ‘I want to put my house on the market in January but … my job doesn’t start until May 1st,’ that would be a different approach than putting your house on the market in January and the job starts February 1st,” said Darden.

According to an Allied survey of 3,500 respondents, 47% of people relocating for a job had thirty days or less to move. Such a tight timeline makes a traditional home sale logistically difficult and you might consider accepting a cash offer for a shorter closing.

Although most sellers choose to list on the open market to achieve the highest possible price point for their house, a cash offer provides simplicity and certainty, so it could be an attractive option to streamline your job transfer.

Need a No-Fuss Home Sale?

Find out what cash buyers are willing to pay for your home right now.

3. What benefits will my new job have and how do they compare to my current employer’s offerings?

Not everything can be compared by salary alone. Glassdoor’s Employment Confidence Survey noted that about 60% of people reported that benefits and perks were a major factor in considering whether to accept a job offer—even over a pay raise.

The Harvard Business Review reported that it had surveyed 2,000 workers ages 18 to 81 about 17 benefits they would weigh when deciding between a high-paying job and a lower-paying one with more perks.

The majority (88%) gave heavy or some consideration to a job with better health, dental, and vision insurance, as well as more flexible hours.

Other benefits that respondents said might influence their job choice included more vacation time, work-from-home options, student loan or tuition assistance, paid maternity or paternity leave, free gym membership, and free day-care services.

4. Can I find a comparable community where I’m relocating?

Getting acclimated to a new community is the second most challenging part of relocating for a job behind finding a new home, according to Allied. If you have children, you’ll naturally have questions about schools in a new area, for instance.

While some companies provide suggestions from all personnel to new employees who are house hunting, ranging from neighborhood commute times to school district ratings, your real estate agent also can be a good resource.

“It’s not just selling their home but answering all those other questions: What is the school district? Where can I go that somewhat parallels where I am now?” Darden said.

5. How far will my new commute be?

According to CNBC, Americans are spending more time commuting to work: about 26 minutes each way compared with less than 22 minutes each way in 1990. Those extra minutes add up throughout the year to a whole work week (about 35 hours) in transit! So consider in your calculations, not just the price of gasoline but any benefits that might offset a long commute, such as flex time.

SmartAsset has a handy commute calculator you can use. Simply input your future home address, work address (plus any other addresses you’d like to compare) and it will give you an estimated commute time by car, public transportation, or foot.

6. Will my employer pay for me to visit the new city and scope it out first?

When you’re relocating to another city or state because of work, your employer might provide financial relief for your moving expenses.

“I would say probably that for at least 50% of my clients, the company picks up a lot of the moving expenses and other costs that are associated with selling their home,” Darden said.

Although Darden has known employers to pay for expenses only to help with the move itself, there are companies that provide other forms of compensation.

According to the Allied survey:

20% of respondents said that their employer sponsored trips for a house search.

21% of respondents received a lump sum to use as needed.

22% received a “miscellaneous expense allowance,” either of which could be used to check out housing once you’ve accepted the job.

7. What moving expenses will my employer pay?

In general, the larger the company, the more likely you’ll have some financial assistance with your move. About 63% of the Allied respondents who had relocated worked for companies that offered relocation packages. Companies with 5,000 or more employees had this benefit in 77% of moves, but even about 71%-72% employers with 500 to 1,000 employees offered a relocation package.

8. What’s my tax liability?

The Internal Revenue Service won’t require you to pay taxes on up to $250,000 of capital gains from the sale of your home if you’re filing as an individual and you’ve used this as your primary residence for at least two of the past five years. (This exclusion bumps up to $500,000 for couples filing jointly.)

Even if you meet that exclusion, however, you may be responsible for municipality and state taxes, depending on the details of your move. Consult an accountant before you file to help you sort through these fees, as well as walk you through deductions you qualify for.

9. What coordination will I need to do between here and there?

Some employers contract with a relocation company that helps employees find and purchase housing in a new area. Darden has known clients who have had such a benefit, which picks a real estate agent in the new location. He’s also assisted people without access to this service by coordinating with another agent from his brokerage in their new hometown.

However your move is structured, you want effective communication. “You want to liaison with the Realtor where they’re going and help with that process,” he said.

Studies consistently show that moving is one of the most stressful events in life, whether you’re moving across town or across the country. But there are resources and professionals available to help take off the pressure by answering your most pressing questions.

“Even if you haven’t found the house yet, you get all the questions answered that you can,” Darden said, “because the more unknowns you remove from a situation, the less stressful it’s going to be.”

Source: homelight.com ~ By: Valerie Kalfrin ~ Image: Canva Pro

Country Living with Views of the Sierra’s. ON the Edge of Town, Quite Road. This Farm House is Approx. 1736sf with 3 Bedrooms and 2 Full Baths. The home has Lots of Character and has been Completely Remodeled with Newer HVAC, Flooring, Inside Paint, Outside Paint, New Kitchen with Appliances, Newer Electrical, and More. It has an Extra Big Office/Media Room. Front Room has Big Windows with Big Views. Detached Two car Garage with 2 Car Carport. Fenced with Pasture and TID Irrigation Water. Perfect Place for you to Raise your Family…

Here’s a look at the process of calculating the value of your home and what it means for your home’s sale price.

You know how much you paid for your home, and you likely factor the work you’ve done and the memories you’ve made there into your idea of what it’s worth. But while your home may be your castle, your personal feelings toward the property and even how much you paid for it a few years ago play no part in the value of your home today.

In short, a house’s value is based on the amount the property would likely sell for if it went on the market.

Why Should You Know the Value of Your Home?

You should have a grasp of the value of your home in a variety of situations: if you’re getting ready to sell your house, looking to refinance your mortgage or buying a new homeowners insurance policy, for example.

For a better understanding of what your home’s value means, how it may change over time and what the impact may be if the housing market shifts significantly in your neighborhood, city or even the whole country, here’s our breakdown.

If your property value is based on what a buyer is willing to pay for it, all you have to do is find someone willing to pay as much as you think it’s worth, right?

Determining a home’s value is a bit more complicated. Keep in mind that buyers place no value on the good times you’ve spent there and might not consider your updated bathroom or in-ground swimming pool to be worth the same amount you paid for the upgrades.

And even if you find a buyer willing to pay $450,000 for your home, the value of your house isn’t necessarily $450,000. Ultimately, the financial backing in a deal determines the property’s value, and it’s most often a mortgage lender making the call.

Property valuation primarily takes into account recent sales of comparable properties in the area. Key identifying factors are the same square footage, number of bedrooms and lot size, among other details. Professionals who determine property values for a living compare all the details that make your house similar and different from those recent sales, and then calculate the value.

But when your property is unique – maybe it’s a triangular lot or a four-bedroom house in a neighborhood full of condos – determining the value can be more difficult.

The individual, group or tool appraising the property may also influence the outcome of the appraisal since they all appraise properties differently for a variety of reasons. Here’s a look at common appraisal scenarios.

Lender Appraiser

In the case of a property sale, the appraisal often happens once the property has gone under contract. The lender will hire an appraiser to complete a report on the property, getting all the details on the house and its history, as well as the details of similar real estate deals that have closed in the last six months or so.

If the appraiser comes back with a valuation below that $450,000 sale price you’ve agreed upon, the lender will likely state that it is willing to lend an amount equal to the property’s value as determined by the appraisal, but not more. If the appraisal comes in at $425,000, the buyer has the option to come up with the $25,000 difference or try to negotiate the price down.

Sellers are often open to negotiation at this point, knowing that a low appraisal likely means the house won’t sell for a higher price once it’s back on the market, though excessive interest in a property may be able to sway an appraiser.

Lindsay Katz, a real estate agent with Redfin in the Los Angeles area, says low inventory and high demand has made the Los Angeles market extremely competitive. In cases of multiple offers on a home that drive the price above its initial asking point, a higher value becomes easier to prove to an appraiser that the market value of the home has risen. “I don’t know how you can’t justify that price when 13 people agree,” Katz says.

Appraiser You’ve Hired

If you haven’t yet put your house on the market and are struggling to determine price, hiring an appraiser can help you get a realistic estimate.

Especially if you’re struggling to agree with your real estate agent on what the most likely sale price will be, bringing in a third party could provide additional context. The cost of a formal appraisal is about $350 on average, according to home services company Angi.

Online Home Value Estimator

Many real estate information sites offer more informal home appraisal tools that will give you a ballpark value for your home. You may have previously taken a look at U.S. News’ own home value estimator, Zillow’s Zestimate, realtor.com’s RealEstimate tool or explored the Federal Housing Finance Agency’s House Price Calculator.

It’s important to keep in mind that an online home value estimator is simply pulling from available information online and may not have all the facts that a professional appraiser would utilize in a valuation report. The online algorithms can catch many details, but they don’t necessarily have the ability to account for more localized factors, like the impact of severe storm damage or trends taking place in your city.

“There’s a lot of information out there,” says Danielle Hale, chief economist for realtor.com. “They don’t always agree, depending on how unique your home is or if there aren’t a lot of sales where your home is.”

Tax Assessor

Your home’s value also determines annual property taxes. In addition to examining the sale prices of similar houses that sold recently, a tax assessor looks at what the cost would be to build a similar house, whether you’ve done any recent improvements, if you earn income from the property and the cost of upkeep.

A property’s assessed value for tax purposes is often less than the appraised value – and that’s a good thing. The property taxes you pay annually are based on the assessed value, so the higher it is, the more you owe.

How Do Market Values Apply to My Home?

There are multiple ways to find out the current value of your house, but individual appraisals and assessments aren’t the only cases where you’ll hear about home values. In annual, quarterly or even monthly reports, home values are often discussed along with the rising cost of homeownership on a local, state and national level.

Depending on the source of information, reported values may be based on online estimator tools, listing prices for houses currently on the market or property value information from local assessors’ offices. These numbers are useful to discuss trends on a large scale, but they don’t always reflect the actual sale prices of real estate deals that closed in those time periods.

The details you get about rising values can be useful as you prepare to put your home on the market, buy your first house or learn more about economic forecasts, but don’t take national trends as indicators of what’s happening in your area.

The importance of trends in home values depends on the stage of homeownership you’re in or moving toward. Here’s what you should know:

As you’re preparing to start house hunting, keeping up on real estate market trends can be an excellent way to know what you’ll be facing. If values are climbing every month and year-over-year comparisons show fast growth – for example, 5% or more – those are signs that a lot of buyers are looking for houses at the same time as you. In mid-2021, home values were climbing at an incredibly fast pace, and the median sale price in the U.S. was seeing more than 20% year-over-year growth. Don’t expect this to repeat soon.

For Investors

Whether you’re looking to invest in a property for rental income or buy a fixer-upper for a quick turnaround, current market trends may influence your choice of purchase. In Los Angeles and many other parts of the country, more time spent at home during the pandemic caused many buyers to shift their focus when looking for a place to live. Instead of prioritizing proximity to shopping and nightlife, for example, “people renting or living in a condo are thinking they’d like to have a backyard, perhaps a pool,” Katz says.

But before you invest in a sprawling property with all the outdoor amenities, learn more about the market and its previous trends. You’ll also want to crunch the numbers to see if rent will be able to cover the mortgage and upkeep on an income property.

If you’re preparing your home for sale or just looking to learn more about your net worth, keep in mind that wider home value trends and reports have little impact on you.

Instead, keep a close eye on local reports; those that provide monthly or quarterly trends on your specific ZIP code can be a better reflection of what’s happening to your property value, Hale says.

Especially if you’re considering selling your home, a knowledgeable real estate agent could be your best source in understanding your property value. “You would want to reach out and talk to an agent and get a local expert’s assessment,” Hale says.

On the other hand, “if you’re not selling, a (positive) change in value still might help you feel wealthier,” says Hale, noting that a current valuation of your home may help you make future financial decisions.

How Can I Increase My Home’s Value?

Whether you’re planning to sell now or in a couple of years, or you’re simply looking to make your home as valuable as possible in the long term, you can potentially help increase its value with regular maintenance, renovations or even additions that could appeal to homebuyers.

Short Term

Many homeowners are motivated to add value to a property when they’re preparing to sell. It’s not impossible to add a couple of thousand dollars to the price tag with some simple remodeling projects that can make your home look fresh and appeal to buyers. Here are a few:

Maximizing value isn’t just about cosmetic fixes – it’s also about focusing on key areas like the roof and HVAC systems that would come up in a home inspection. Issues like leftover water damage on the ceiling from an old roof leak or a cracked window will show up in the home inspector’s report. If anything concerns the buyer too much, you may run the risk of the deal falling through.

Midterm

If you’re looking to make changes to your home so it’s on par with a different caliber of properties in your neighborhood, consider these larger construction projects:

These more extensive changes can be an excellent way to take your home to the next level, but only if other houses like this exist in the area. Adding a master suite and new garage to a neighborhood full of two-bedroom bungalows with street parking won’t make the property appraise much higher than the others. That’s because your house may no longer appeal to the typical buyer in that neighborhood.

Long Term

If you’re looking to increase your home’s value for the sake of your overall wealth, the best thing you can do is continue to pay off your mortgage and gain equity in the property. With proper upkeep and work to keep the home up to date, your home value will, on the whole, naturally increase over time.

$499,900 – Ready and Ready… This Semi-Custom home is Approx. 1734sf with 3 Bedroom and 2 baths. Updated Kitchen with Counter Tops, Backsplash, and Painted Cabinets. Laminate Flooring Throughout with New Paint, New Carpet, New Appliances, New Grass, and New Garage Floor Paint. Great Design and with High Ceilings. Big Open Family Room with Large Fireplace. Cozy Formal Dining Area. This home is Light and Bright with Views. Inside Laundry. Down the Street from Markley Park. A Must See!

Property Features

Bedrooms

Bedrooms: 3

Primary Bedroom Features: Outside Access

Appliances

Equipment: Dishwasher, Disposal, Microwave, Free Standing Electric Oven

9527 Meadow drive.. What a View!! Approx. 3.4 acre Ranchette on a Hilltop, Overlooking the Central Valley, and the Merced river. Custom designed Home of Almost 2500 ft. with 3/2.5 with a Possible 4th Bedroom. Many Custom Features from Views, to Wood-Work, to Design Details, and More. There’s a Loft, Media Room, and a Private Balcony off the Kitchen Nook. Master Bath and Kitchen were Remodeled in Recent years, Newer Black Top Driveway, and More. Lots of Privacy, Big Trees, Many Fruit Trees, and a Big Pool with lots of Decking to Entertain. Big Backyard with Grass and Basketball Court. Big Barn of Approx 33×36 Barn w/ 3 Roll up Doors and a Separate 33×60 Carport-Overhang for Storage or a Shop Conversion. MID Irrigation Water Available to this Parcel. There’s is Room For to Setup for Animals or Another Shop. A Very Special Place with Privacy and Views!! A Must See!!

Going solar in California could be worth it even with the state’s new net metering rules.

California is a leader in the solar industry, with enough solar power installed statewide as of December to power 10.7 million homes. Solar panels may be a good option if you live in the Golden State and are interested in lowering your household carbon emissions while also saving on energy bills.

California’s average residential electricity rate is higher than the national average making Californians pay a higher traditional energy bill than residents in other states, according to SaveOnEnergy, CNET’s sister company.

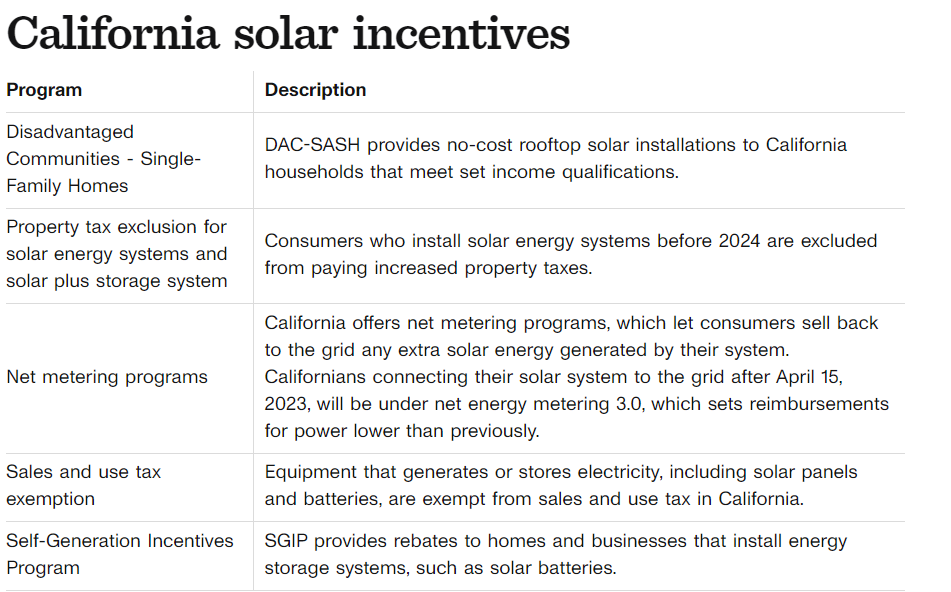

On April 15, California’s new net metering regulations went into effect. Overall, they increase the incentives for going solar with a battery while reducing the payouts for solar without storage.

Meanwhile, the cost of residential solar panels has decreased by more than 69% in the last two decades, according to a Lawrence Berkeley National Laboratory report. Tax credits and rebates at the federal, state and local levels can help bring that cost down further. Whether you’re interested in helping the environment or lowering your energy bills, the amount you could save on solar panels in 2022 is higher than in previous years.

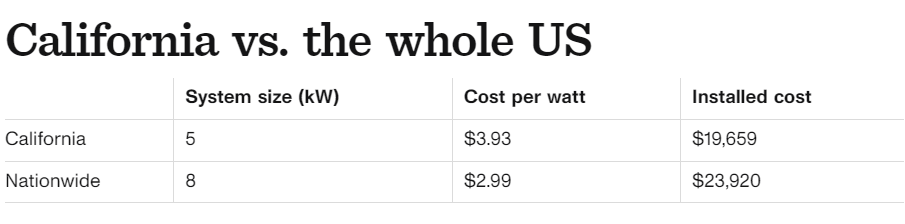

California solar panel costs

The cost of a home solar panel system will depend on the system size (i.e., the number of panels included), components like solar batteries and installation costs. California’s average solar panel system is smaller (and therefore cheaper) than the national average, even though the cost per watt is normally above the US average.

Because solar is so popular in California, there is also a high number of solar panel installers, which gives customers plenty of options to choose from when looking for the right solar company.

Here’s a breakdown of the average size and cost of solar panels in California and nationwide based on 2022 data from Findenergy.com and consulting firm Wood Mackenzie.

How to pay for solar panels in Californ

If you decide to invest in solar panels for your home, there are several financing options to make the purchase easier.

Cash: A big expensive project like solar panels requires a lot of cash. If you see solar power in your future consider saving money now. Regular contributions to a high-yield savings account can help pad your savings.

Solar loan: Many solar companies will offer third party financing. Shop around with different lenders, because your solar company’s third party choice might not have the best terms or interest rate.

Home equity loan or HELOC: You can also consider a home equity loan or line of credit,. These can save you on interest but your home is at risk if you fail to repay.

Mortgage: Another way to get the cash for solar panels is to refinance your mortgage. Fannie Mae’s HomeStyle energy mortgage is designed to fund energy efficiency projects.

The residential clean energy credit (previously known as the investment tax credit) is a federal solar tax incentive offered in California that credits 30% of the cost of a solar system back to consumers who buy solar panels. This solar tax credit was increased and extended due to the Inflation Reduction Act, passed in August. There is no cap on the federal tax credit, so you can claim the entire 30% regardless of the size of the system.

You can apply for the residential clean energy credit by including IRS Form 5695 with your tax return. The IRS provides instructions on how to fill out this form, or the best tax software can take care of it for you. Your savings from the tax credit will be included in your tax refund or used to offset taxes you owe.

According to the Solar Energy Industry Association, nearly 2,000 solar companies operate across California. While this means there are plenty of California solar installers to choose from, it can also feel overwhelming to sort through your options.

We’ve compiled a list of solar panel companies that stand out in the industry. Here are a few California solar installers you can consider during your search.

ADT Solar

Formerly Sunpro Solar, ADT Solar operates throughout California and provides a variety of solar systems, including battery installations. ADT Solar says it prioritizes customer satisfaction and offers 25-year labor, power production and manufacturer warranties. The company also extends a price-match guarantee on installations.

ADT Solar does not offer solar leases or PPAs. It previously preferred to source its solar panels from LG, which left the industry in 2022. Since then, ADT Solar has confirmed it is committed to providing solar customers with a 25-year manufacturer warranty and will continue to extend a 25-year production guarantee from ADT.

Palmetto Solar

Palmetto is one of the largest solar companies in the country and offers home solar systems in California. With Palmetto, you can buy solar panels outright or sign a solar lease or PPA. The majority of Palmetto’s customers choose to buy their solar system to save the most money on energy bills over time.

Palmetto has operated in the solar industry since 2010 and says it’s committed to top-tier customer service. It offers a subscription called Palmetto Protect, which monitors the performance of a solar system and provides tiered levels of support if the solar panels are damaged or fail. Palmetto solar panels have an efficiency rating above 19.8%, a minimum 12-year product warranty, and a 25-year performance guarantee.

SunPower Solar

SunPower offers some of the most efficient residential solar panels and the best warranties on the market. With an efficiency rating of up to 22.8%, the SunPower Equinox solar panels outrank all competitors. The SunPower Equinox package includes solar panels from Maxeon, a manufacturer that worked with the company until 2020, and Enphase microinverters and mounting equipment.

SunPower operates across most California regions and aims to continue providing more accessible and affordable solar products. The company was founded in 1985 and offers some of the strongest warranties available, guaranteeing 92% production capacity for 25 years.

Sunrun

Sunrun is the largest solar company in the US and offers a strong lineup of solar products and warranties. Sunrun’s focus is on solar leases, which come with a different set of pros and cons, but can be a good option for consumers who aren’t able to purchase a solar system. While most of Sunrun’s customers lease their equipment, the company still offers the option to buy solar panels.

The company currently sources its solar panels from several manufacturers. For people who lease their system from Sunrun, the company provides “bumper-to-bumper” coverage on maintenance and monitoring. However, those looking to buy a system will rely on the manufacturer’s warranties. Sunrun does offer a 10-year quality warranty, which covers roof damage and installation issues.

Tesla Solar

Tesla became a big player in the solar market in 2016 when it purchased SolarCity, which significantly increased Tesla’s installation capacity. Between the solar panel branch of Tesla and the Tesla Solar Roof, Tesla is one of the most recognizable brands in the industry.

The price tag, efficiency rating and warranty terms will differ depending on the solar system you buy from Tesla. The Tesla Solar Roof comes with a 25-year product warranty and a performance warranty at 95% capacity after five years and 85% after 25 years. However, the Solar Roof has a much higher price tag than many competitors.

Meanwhile, Tesla solar panels are more affordable than the Solar Roof, and the quality remains high. Its solar panels are warranted at 85% capacity after 25 years and have an efficiency range between 19.3% to 20.6%. It is worth noting that some Tesla customers have reported issues with customer service.

Installation factors to keep in mind

Solar panels are a big investment, so it’s important to consider all elements that could impact whether they’re right for you. Some installation aspects to consider include:

The condition of your roof: The size, shape and slope of your roof can affect how much electricity a solar system generates. According to the Department of Energy, solar panels are most efficient on roofs with a slope between 15 and 40 degrees. The age and overall condition of your roof are also considerations. Older roofs or roofs needing maintenance should be replaced or repaired before solar panel installation.

HOA and neighborhood regulations: California law prohibits homeowner associations from banning solar panel installations, but there may still be specific requirements and approval processes in your neighborhood. Be sure to research the requirements for solar installation in your neighborhood ahead of time, so there are no issues down the road.

Insurance coverage: After installing solar panels, contact your homeowner’s insurance agency to add the panels to your policy. Most standard homeowner’s policies cover rooftop solar panels, but you’ll need to check with your agency for the specific details of your policy.

Your location: Solar panels are designed to work in all climates and areas that receive indirect sunlight. But they’ll be much more efficient when installed where they receive at least four hours of direct sunlight each day. If your home is in a cloudy region of California or gets shade coverage throughout the day, a solar panel system will not generate as much electricity as it would with direct sunlight.

Rentals: If you rent your home, you may not be allowed to install solar panels. You can check with your landlord or rental management company to confirm whether solar panels are allowed. If not, you can consider community solar programs as an alternative. These let you subscribe to electricity produced by solar panels at another location and receive a credit on your energy bills. The subscription fees are set at a lower rate than the value of these credits, so you come out ahead financially. In California, community solar programs are expected to grow quickly due to new regulations.

Source: cnet.com/home ~ By Caitlin Ritchie ~ Image: Canva Pro

$379,900 Almost an Acre!! An Investment with a House in City of Turlock. Over 40, 000sf LOT Currently Used as a Residential Ranchette. The Proposed Zoning is Commercial/Office Zoning. The Home is Currently Rented, over 1200sf with 3 Bedrooms and 2 Full Baths. The Parcel is Long and Deep, Down the Street from the Hospital and other Medical Businesses. Futhermore, it’s Around the Corner from Offices, Downtown, and further Support Businesses. Lots of Land to Build your Business-Store Front and/or Investment.

Property Features

Bedrooms

Bedrooms: 3

Appliances

Equipment: Free Standing Gas Oven

Laundry Facilities: Inside Area

Heating and Cooling

Cooling Features: Ceiling Fan(s), Window Unit(s)

Heating Features: Wall Furnace

Bathrooms

Full Bathrooms: 2

Bathroom 1 Features: Shower Stall(s)

Interior Features

Interior Amenities: Main Level : Bedroom(s), Living Room, Full Bath(s), Kitchen

Flooring: Carpet

Kitchen and Dining

Dining Room Description: Space in Kitchen

Kitchen Features: Other Counter

Land Info

Lot Description: Landscape Front

Lot Size Acres: 0.9275

Lot Size Dimensions: Approx. 40, 401sf

Lot Size Square Feet: 40402

Garage and Parking

Garage Spaces: 1

Garage Description: Garage Facing Front

Homeowners Association

Association: No

Calculated Total Monthly Association Fees: 0

School Information

School District: Stanislaus

Other Property Info

Source Listing Status: Active

County: Stanislaus

Cross Street: E.Hawkeye Ave.

Directions: Highway 99 to Fulkerth-east. Fulkerth turns into Hawkeye. Left on Olive. Second Property on the Left.