If you’re buying or selling a home right now, one question is likely on your mind: Who holds the power in today’s market?

After years of sellers calling the shots, the balance is edging back toward buyers.

Inventory has risen 10% year over year for the 27th straight month; though, on a monthly basis, active inventory fell 6.8% since December, according to the Realtor.com® January Monthly Housing Trends Report.

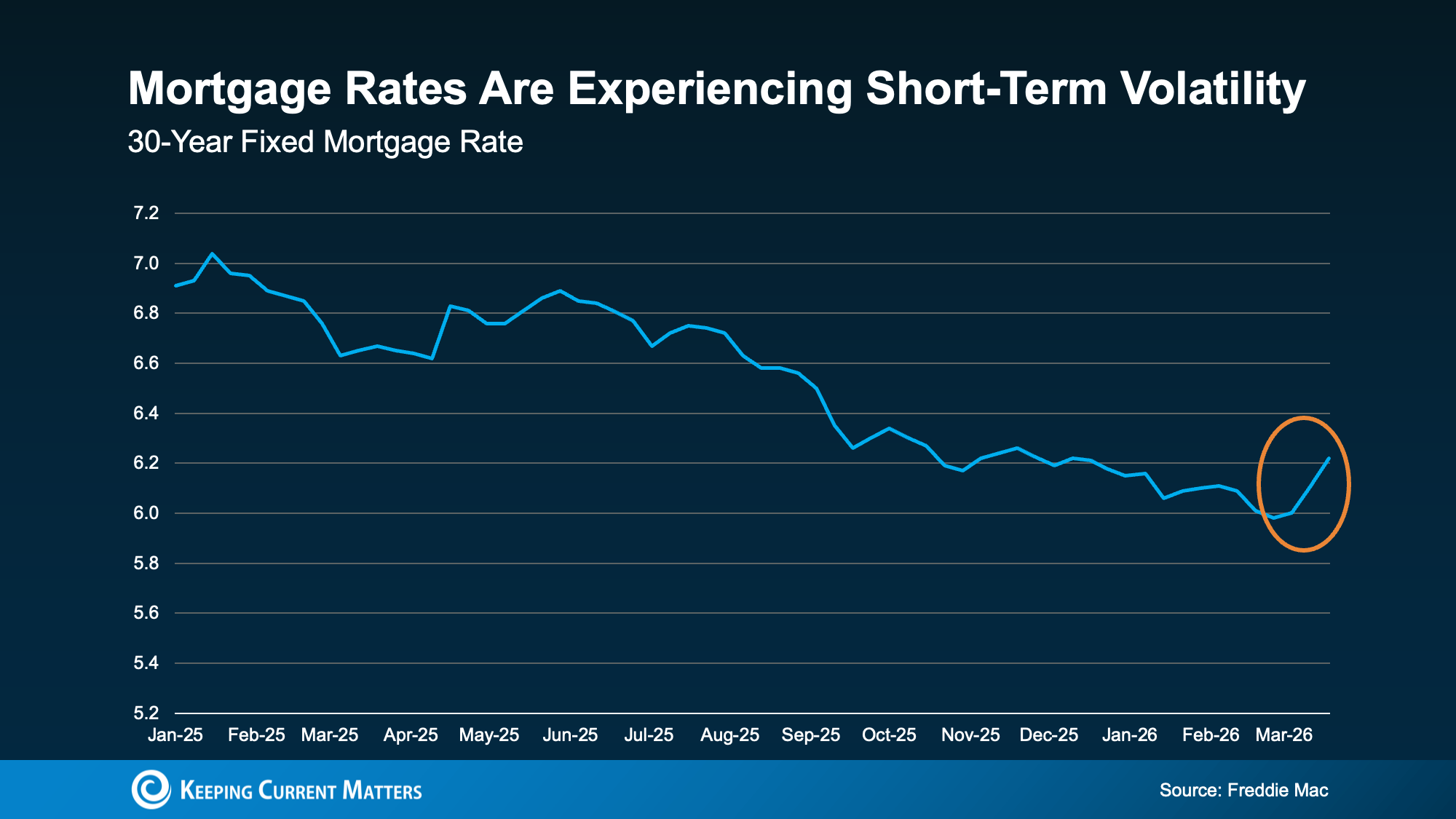

Buyer activity certainly increased in January, as pending home sales—listings under contract—grew by 1.2% year over year, but that number could continue to increase in February and March as mortgage rates finally hit a three-year low and actually fell below 6% on Feb. 26.

The signs are pointing to a more buyer-friendly market more than ever, which aligns with the Realtor.com forecast for 2026. Here’s how to read the signs and navigate this point of flux, whether you’re buying, selling, or just watching and waiting.

What does a buyer’s market mean?

In the simplest terms, a buyer’s market happens when the number of homes for sale exceeds the number of active buyers. This shift in supply and demand gives buyers more leverage as sellers compete to outshine one another.

That means more choices, more room to negotiate, and often, more time to decide for buyers.

This is a notable contrast from the seller-dominated market that’s defined much of the past decade. Since the aftermath of the 2008 financial crisis, new-home construction lagged far behind demand, and buyers competed fiercely over limited inventory.

But in today’s slowly shifting market, the balance of power is beginning to tilt, even if it hasn’t full

Indicators of a buyer’s market

How do you know when the housing market is tipping toward buyers? There are several key signals:

High inventory

“The best single indicator for this is months supply,” explains Danielle Hale, chief economist of Realtor.com. “Typically, months’ supply above six months is the hallmark of a buyer’s market.”

To her point, newly listed homes edged up 0.7% year over year and surged seasonally from December, while pending sales rose 1.2% year over year—their strongest annual gain since late 2024

Active listings are still 17.2% below pre-pandemic norms, though, the widest gap since spring 2025

“Homebuyers and sellers can also look for other clues that go hand in hand with a buyer-friendly shift,” says Hale.

Location offers a significant indication: Inventory grew year over year in 46 of the 50 largest metro markets. Only Jacksonville, FL, San Francisco, Chicago, and Grand Rapids, MI, saw a very slight decline in active listings. Seattle experienced the most notable surge (+32.4%), followed by Charlotte, NC (+28.6%), and Washington, DC (+26.8%).

All of this means buyers are finally seeing more options, but not everywhere—and not evenly.

Slower sales

Homes are taking longer to sell across nearly every region. In January, the typical listing spent 78 days on the market—five days longer than a year ago. It was the 22nd consecutive month of slower sales.

“In a buyer’s market, sellers can typically expect it to take longer to sell a home, and they may have to reduce their home price—either directly in the listing or by accepting a below-asking-price offer—to ultimately make a sale,” explains Hale.

This is advantageous for buyers, explains Hale.

“Buyers can expect that they will not only have more options to choose from, but also have more time to consider their choices,” she says.

But it comes with a major caveat, says Realtor.com senior economist Jake Krimmel.

“Delistings are growing faster than inventory overall, and in some markets, for every two or three fresh listings, one home is being pulled.

“It’s a way for sellers to reassert control in a market where their leverage is fading,” he adds.

Price drops

With listings lingering, price cuts have become a defining feature of the market. Price cuts slightly decreased year over year, with 14.3% of listings discounted, down from 15.6% in January 2025.

Discounts are most common for homes in the $350,000 to $500,000 range, where affordability pressures are sharpest and sellers are more motivated. At the luxury end—$1 million and up—price reductions remain relatively rare as high-end sellers hold out for the right offer.

Concessions

More motivated sellers can also show up in concessions. Mortgage broker Carlos Scarpero has seen a growing number of sellers offer financial perks to seal the deal.

“Even within cities and price points, trends can vary,” he explains. “I’ve closed several deals in 2025 with $10,000 or more in seller concessions. This is certainly higher than I have seen in years past.”

While these indicators vary by region and price tier, the pattern is becoming clear: Sellers are no longer in complete control, and buyers are starting to regain ground.

Is it a buyer’s market right now?

It depends on where you are.

When measured by months of supply, Miami, Austin, TX, and Orlando, FL, rank as the strongest buyer’s markets right now. Tampa, FL, New York City, Las Vegas, and Riverside, CA, follow, respectively.

While buyers may have more leverage in these cities, real estate experts warn that it won’t be felt evenly across all segments of the market. Miami is a strong example.

While demand for condos priced below $500,000 has plummeted, single-family homes remain near impossible to find. On the off chance one hits the market, you’re likely to get burned treating it like a condo.

In other words, “know your segment,” Ana Bozovic, a Miami-based real estate agent and founder of Analytics Miami, told Realtor.com earlier this month.

The same can be said of the national housing market, which is in perfect balance right now. That means more buyer-friendly conditions than there have been in years.

“We’re continuing to see the market shift in favor of buyers,” says Matt Ryan of Bozeman Real Estate Group. “In Bozeman, MT, inventory has finally returned to pre-COVID levels, giving buyers more choices and negotiating power. I expect this trend to continue.”

That buyer-friendliness is showing up at the local level, too.

“It’s definitely been tipping in the direction of buyers lately,” says Brooke Nelson, a ReeceNichols agent in Kansas City, MO. “Showings have really slowed down.”

And in some markets, the shift is already playing out in negotiations.

“Every buyer I’m working with that makes an offer is getting a contract accepted,” notes Mason Whitehead, a branch manager at Churchill Mortgage.

Local and regional variations matter most

While national headlines might suggest a buyer’s market is taking hold, the reality on the ground depends heavily on where and what you’re trying to buy. Local trends can diverge sharply from national averages, especially when you factor in price range, property type, and post-pandemic market dynamics.

In some high-demand pockets, homes are still moving quickly, especially if they’re priced right and well-prepared.

“Buyers have the most negotiating power in the condo market,” explains Aaron Buchbinder, a broker with Compass in South Florida. “On the flip side, single-family homes in prime locations are still seeing strong interest and less flexibility.”

That kind of split isn’t unique to Florida. In many metro areas, buyers might find leverage in one segment while still facing competition in others.

While national stats offer a useful snapshot, the real leverage is local. Buyers and sellers alike should compare today’s conditions with their market’s own history, not just the national narrative. What seems like a cooling market in one city might still be red-hot in another.

What to do if you’re a buyer

With market conditions starting to tilt in buyers’ favor, now might be the time to act, but strategy still matters. After all, competition hasn’t disappeared entirely. Here’s how to make the most of your position:

Get pre-approved

Even in a cooling market, speed can make or break your offer, especially in competitive neighborhoods or price tiers. A pre-approval letter shows sellers you’re serious and ready to move.

Watch the days on the market

Homes that have lingered on the market are increasingly ripe for negotiation.

“Buyers should not be concerned with higher days on market,” says Melissa Bailey, a top agent with the Jason Mitchell Group. “Go see the home that has been listed for 62 days. It could be your home!”

Use contingencies and timing strategically

In a more flexible market, buyers can regain tools they were often forced to waive, like inspection or appraisal contingencies.

“Right now, the biggest advantage is the ability to buy and sell at the same time—sellers are more open to contingent offers and willing to negotiate,” explains Ryan.

Being flexible with closing dates or offering quicker timelines can also help you stand out without raising your offer price.

Stay up to date

Understanding local inventory trends, median days on the market, and pricing patterns can help you recognize when a listing is overreaching and when it’s genuinely a deal.

In today’s market, knowledge is leverage, and a well-informed buyer can often win without overpaying.

What to do if you’re a seller

While the market might be softening, it’s still a solid time to sell if you adjust your approach to today’s more selective buyers. Here’s how to stay competitive and avoid sitting on a stale listing.

Price realistically

Gone are the days of aggressive overpricing and instant bidding wars. Today’s buyers are more cautious and cost-conscious.

“Sellers who were unrealistic in Q1 are adjusting to today’s buyer expectations,” says Darin Tansey, director of luxury sales at Douglas Elliman.

Listing high in hopes of negotiation room could backfire, especially with inventory rising. A well-priced home will attract more attention and better offers upfront.

Prepare your home well

Buyers are still drawn to clean, move-in-ready homes, and the basics still matter. Invest in staging, photography, and curb appeal. A strong first impression can make the difference between a quick offer and weeks of radio silence.

Know your market

In some areas, homes are still moving fast. In others, they’re lingering. The more your agent understands local demand, the more they can guide pricing, marketing, and timing strategies.

Don’t panic

Yes, buyers are gaining leverage, but that doesn’t mean you’re at a disadvantage.

Adjusting to this new reality doesn’t mean giving up value; it means staying nimble. Well-prepared, fairly priced homes are still selling, and in many areas, sellers remain in the driver’s seat, just with a lighter grip on the wheel.

A shift, not a flip

While it might seem like the market is suddenly favoring buyers, the reality is more nuanced.

“We’ve been in a seller’s market pretty consistently since 2016, when months’ supply averaged 4.4 months across the year. Since then, it’s averaged four or lower, signaling a tough market for buyers. Given the persistence of underbuilding relative to housing demand over the last decade, it’s not surprising that we have been through a really persistent seller’s market,” says Hale.

After years of seller dominance, conditions are gradually becoming more favorable to buyers. Inventory is up, price cuts are more common, and homes are taking longer to sell. But in many markets, especially in desirable neighborhoods or lower price tiers, sellers still hold meaningful leverage.

“While some are calling this housing market a buyer’s market, I would say that it’s more of a market in transition,” says Hale.

That means that while sellers won’t need to sacrifice all their power, they will need to adjust expectations.

“It is not realistic to expect multiple offers pushing home prices over market value,” says Missy Derr, a real estate adviser with Engel & Völkers in Atlanta. “Buyers finally have more than a fair shake at securing a home.”

Whether you’re buying or selling, this isn’t the time to rely on headlines alone. The national market might be cooling, but the story varies neighborhood to neighborhood. That’s why it’s more important than ever to watch local trends, compare current conditions to pre-pandemic norms, and work with an agent who understands the intricacies of your area.

Source: realtor.com ~ By Allaire Conte ~Image: realtor.com