SOLD – 42 ac Monte Vista Avenue, Denair

209-988-5254 | Century21 Select | DRE #01225017. – Serving Stanislaus, San Joaquin & Merced Counties.

You can build equity faster with a shorter term since more of your payment goes toward paying down principal.

If you’re preparing to buy a home, you will need to look at not only mortgage interest rates, but also loan types and terms. Your mortgage term is how long you have to repay the loan, and most terms are 15 or 30 years.

Should you get a 15- or 30-year mortgage? If you can afford the payment on a 15-year mortgage, the long-term interest savings are great. But the lower monthly payment of a 30-year mortgage could offer you more flexibility if your financial situation changes.

Here, we break down the 15- vs. 30-year mortgage debate, including the pros and cons of each and how to decide between the two.

The primary difference between a 15- and 30-year mortgage is the length of time to pay off the loan.

A 15-year mortgage pays off your home in half the time of a 30-year loan and saves on interest overall. Borrowers typically qualify for lower interest rates for 15-year loans because the shorter term reduces risk for lenders.

The shorter term also means that more of your payment goes toward paying down principal, so you can build equity faster than with a 30-year mortgage. The trade-off is a higher monthly payment than a 30-year mortgage – at current rates, 20% or more. “The higher costs may not leave room for additional homeownership costs, such as renovations or unexpected repairs and maintenance,” says Shelby McDaniels, national director of business development at Chase Home Lending.

A 30-year loan’s lower monthly payment can provide more cushion in your budget. This can help make homeownership a possibility for more people.

Pros

Cons

Pros

Cons

Let’s say you need a $300,000 mortgage and qualify for a 15-year at 6.5% or a 30-year for 7.5%. Here’s how those costs would compare:

| 15-Year | 30-Year | Difference | |

| Monthly Payment | $2,613 | $2,098 | $516 savings per month if you choose a 30-year mortgage |

| Total Interest Paid After Full Term | $170,398 | $455,152 | $284,754 savings in total if you choose a 15-year mortgage |

| Total Loan Amount After Full Term | $470,398 | $755,152 |

If you’re on the fence between a 15-year and a 30-year loan, some lenders offer terms in the middle, such as a 20- or 25-year mortgage term. There are even some companies with 10- or 40-year terms if you’re looking for even more flexibility. Ask your mortgage professional to run the numbers to see which term option is best for you.

“There are tricks and hacks to dramatically reduce interest over the loan term,” says Erik Katz, president and founder of Rustic Country Real Estate in West Point, California. “If you take a 30-year loan and pay a few extra hundred a month, you may pay that mortgage down in 15 years anyway.”

Katz also suggests making an extra full payment at the end of each year if you can swing it to make a nice dent in the principal. You can also set up mortgage payments every two weeks, which results in an extra payment per year.

This way, if things ever get tight financially, you’re not locked into a higher payment. Just confirm that your lender doesn’t charge a prepayment penalty.

Starting off with a traditional 30-year term is best for many people. But if circumstances arise a few years into the mortgage that might allow you to refinance to a 15-year loan, such as a dramatic drop in interest rates, it could be worth exploring.

On the flip side, if you start out with a 15-year mortgage and the payments become difficult to manage, you can see if stretching it out into a longer loan term might help ease the financial pressure. Just be aware that doing so will mean paying more interest over the life of the loan.

Deciding between a 15- or 30-year mortgage comes down to finances and flexibility. Keep in mind that 30-year mortgages are far more common than 15-year loans for a reason: They are more affordable. The lower payment will give you more wiggle room, especially if your financial future is uncertain or your dream home wouldn’t be within reach with a 15-year mortgage.

On the other hand, a 15-year mortgage can offer savings if you have steady income to support your monthly payments and other expenses, including emergencies. “If the interest rate is a lot lower for the 15-year, that’s where I would advise to run the numbers,” says Katz.

Age may be a factor in your decision when weighing a 15- versus 30-year mortgage as well. “A 15-year mortgage could be a better option for those who are determined to pay off additional debts quickly, especially those who are preparing for an early retirement and want to minimize monthly payments,” says McDaniels.

A 40-year-old borrower, for example, could pay off a 15-year mortgage by age 55 while still owing on a 30-year mortgage through age 70.

If your ultimate goal is to save money, says Katz, “the name of the game is how fast can you get your house paid down.” Do the math and calculate your potential mortgage payment before you decide.

Source: money.usnews.com ~ By Dawn Papandrea ~ Image: CanvaPro

Welcome to Hilmar Gold!! This Perfect Family home features Approx. 1524sf with 3 bedrooms, 2 baths on a Large Corner Lot. Great Room Concept with large Family Areas, Soaring Vaulted Ceilings, Cozy Brick Fireplace, And Formal Dining area. Updated Kitchen with Granite counters, Stainless Appliances, and Stylish Tile Floors. Backyard is very accessible from the Corner Lot. Tool Shed, Garden, Fire Pit, and Large Patio Area with additional Outdoor Living Space.

Buyers have all kinds of schedules and you may sometimes need to show your house at the last minute, depending on the kind of market where your home is listed.

Buying a house was one thing, but now you’re ready to upgrade, and you have to sell that house while you live in it. It’s a problem a lot of homeowners face, and although selling your home while you’re living in it can be a challenge, it’s not an impossible situation.

In fact, it’s common for sellers to live in their house until they sell it. But to do it successfully, you’ll need a plan to keep your living space tidy and ready to show to buyers.

Getting your house ready to show requires thinking like a buyer. No one expects you to live in a museum, but you should consider the impact of your belongings and lifestyle on potential buyers who may come in to look around.

“Everyone sees things differently,” says Désirée Ávila, real estate agent at Charles Rutenberg Realty Fort Lauderdale in Fort Lauderdale, Florida. “Some like to see it with the current furniture, while others prefer to see it empty so they can imagine their own furniture in it. That being said, a tip I always give clients is to declutter and depersonalize. Make the house look neutral, kind of like a hotel room.”

Although most people with families and busy schedules can live a bit of a chaotic life behind closed doors, it’s important to develop a system for containing all the mess that comes with being a person before you start showing your home. Buyers often make decisions based on their impressions, regardless of how great your house is under the necessary layer of lifestyle.

“Leaving mail on the counter, dishes in the sink, etc., makes the house look messy, smaller and oftentimes gives the impression the house is in worse shape than it is,” says Rick Albert, broker associate and investor with LAMERICA Real Estate in Los Angeles. “In residential real estate, there is a lot of emotion and feelings. It trumps logic more than people will admit.”

Realtors will tell you to declutter, but they rarely go into great detail about what that means. For someone who is naturally a little cluttery, it can be hard to know when you’ve reached the peak decluttered point.

“Try to reduce every surface (countertops, dressers, coffee tables) by a third,” says Ginger Lazovik, real estate agent with the Falk Ruvin Gallagher Team of Keller Williams in Milwaukee. “A good rule is three items per surface. Make sure that each surface is free of clutter and has no more than three essential or decorative items on it. Next, downsize the items in your closet and cabinetry by half. When buyers tour, they open closets and cabinets. Overstuffed cabinetry makes your home look like it does not have enough storage.”

But where do you put all that stuff you need to remove temporarily, but don’t want to get rid of permanently? A lot of sellers will automatically rent a storage unit, but real estate professionals say that’s not always a necessary expense if you have suitable storage space in your home and not too much decluttering to do.

“If sellers are able to neatly store their boxed items in the garage, basement, or extra room in the home, a storage unit may not be necessary,” says Jessica Fisher, real estate agent with RE/MAX Professionals in Cottage Grove, Minnesota. “Potential buyers are forgiving of boxes as long as they are neat, tidy, and not hindering their ability to examine the space.”

You may have heard that a home needs to be professionally staged to sell. This is not necessarily true. When you’re living in a home that you’re selling, people understand that you still live there. It’s still important to make your home seem very appealing.

“A well staged home can include the owner’s personal furniture,” Lazovik says. “Make sure that you do not have too many pieces of furniture in any particular room. Remove overstuffed chairs or anything that looks worn or damaged. Add layers like cozy pillows and fresh blankets and throw rugs to freshen up your space. Fresh flowers add color and a clean smell.”

The money you save on staging can pay off big time if you spend it on improving the first impressions of your home. After all, if people drive by, but aren’t interested enough to walk through the front door, you’ll never sell your house.

“The outside is the first impression a buyer will get of the house,” says Ávila. “As the old saying goes, you never get a second chance to make a good first impression. Investing in making the outside look inviting is essential, otherwise some buyers may choose to pass on the house altogether.”

Once your house is ready to show – really ready – it’s time to figure out how to keep it in show-ready condition. Buyers have all kinds of schedules and you may sometimes need to show your house at the last minute, depending on the kind of market where your home is listed.

“The kitchen and bathrooms must look impeccable. Always close the toilets and pull the shower curtain,” says Ávila. “Little Johnny might not like to make his bed but it is important that it is made if showings are expected. If the realtor gets a call that there is a cash buyer willing to close quickly, if the seller really wants to sell, they need to be ready to make an exception (to their showing schedule). If little Johnny’s bed is made, that is one less thing to scurry about doing to get the house ready for a showing not during the regular showing schedule.”

Other things to consider when preparing for showing are children’s toys and pets, both of which can make a house very hard to show if they’re not kept up with. If your child is too young to keep their toys completely picked up, or you can’t take the dog for a walk during every showing, there are options.

“What I have done is asked that kids’ toys be in a designated area, rather than all over the place,” says Albert. “For example, maybe the toys can all stay in the kid’s bedroom. For pets, gate off the side of the house and the pets can hang out there during the showing.”

The idea that it’s a buyer’s market everywhere is fading, and there’s a lot of differentiation starting to take place. Understanding your market will help you set your expectations.

“For years, the country was moving in lockstep – it was a seller’s market everywhere,” says Lazovik. “Now, depending on where you live, it is either a buyer’s market, like Austin, a neutral market, or still a seller’s market, like Milwaukee.”

There are lots of different markets even within a single metro area, but your agent can give you some idea of what has happened with houses like yours and get you ready for what’s to come, whether that’s a chaotic cluster of showings that will feel like you’re in a war zone, or something a bit slower.

“The Twin Cities is currently experiencing what I call ‘A Tale of Two Markets,’” says Fisher. “Homes at $350K and below that are priced and presented well still have a chance at several showings and multiple offers. The move-up home market is much different. Sellers with homes priced above $350K can expect fewer showings and longer days on the market because this buyer pool typically has a home to sell first or is reluctant to give up their current lower mortgage rate. Although we don’t have the ability to see the future, we as agents try to prepare each seller for their specific situation.”

Source: realestate.usnews.com ~ By Kristi Waterworth ~ Image: Canva Pro

How long it takes to sell a house depends on numerous factors. Here’s a look at the typical home-selling timeline.

Key Takeaways:

Every homeowner’s home-selling journey is unique, even in terms of the time it takes to close the deal. In some cases, it could take just a matter of weeks from when it’s listed to closing, while others could sit on the market for months before going under contract. How long it takes to sell a house depends on your local market conditions, demand, the decisions you make and how you approach the selling process.

As of February 2025, the median days on market, or the number of days a home sat on the market before going under contract, was 54 days, according to real estate brokerage Redfin. Between Feb. 10 and March 30, the median number of days to close on a home after going under contract was 24.5 days. That totals 78.5 days on average from listing to closing; however, the sale of your home could be different. Every market and individual sale will vary in terms of the number of days on market and the time it takes to close.

While some houses may sell quickly, others can take longer. Once a house is listed, several factors can influence the speed of the sale. Here are some of the biggest factors to consider.

The law of supply and demand plays an important role in the real estate market on a national and local level. The state of the market is typically expressed as a buyer’s market or a seller’s market.

In a buyer’s market, there’s a bigger supply than there is demand for housing. It typically takes longer to sell in a buyer’s market. In a seller’s market, the demand exceeds the supply. Homes sell faster and sellers can command a higher asking price. A balanced market is one with four to six months of supply.

Buyers tend to be more cautious of homes that have been on the market longer than others. “Buyers start to wonder what is wrong with the property and may pass it over for another property that hasn’t been available as long,” says Jessica Fisher, a licensed real estate agent in Minnesota and Wisconsin.

Pricing your home too high can result in fewer offers or offers coming in considerably under the asking price. “In this market, homes are selling quickly if they are appropriately priced,” says Fisher. “Over-pricing presents challenges, including the stigma that comes with a home being on the market for any length of time.”

Potential buyers may overlook a home that needs extensive repairs. This could lengthen the time a house sits on the market. Uncovering problems with the home could also lead to additional negotiations and concessions that may impact the selling timeline.

Location is key in how long it takes to sell a house and the property’s perceived value. If the house is in a highly desirable location, then it could sell quickly. If it’s located in an undesirable neighborhood, it could take longer.

There are several steps to the home-selling process. Here is the typical timeline and how long each step usually takes:

If you’d rather not spend the time and effort selling the home yourself, a real estate agent can help you through every part of the home sale.

“The first thing a homeowner should do is contact a trusted Realtor,” says Fisher. “A Realtor will be able to give the homeowner a clear picture of what’s happening in the local market and will also be able to provide a market analysis of the home, discuss pricing strategies and explain the sale process from start to finish.”

It’s also important to compare and interview agents in your area. “Sellers should hire an agent that honestly communicates with them about the market value of their home, the process of selling and what to expect. You want an agent to tell you the good, the bad and the ugly no matter what happens,” Fisher says.

Unless you decide to sell your house as is, you need to prepare it to be listed on the market and shown to potential buyers. The length of time it takes to prepare the home will depend on how much maintenance and work the owner has already put into it.

According to the Bright MLS survey conducted in December 2024, more than half of buyers (56.1%) said that it was “very important” to buy a move-in-ready home over one that requires any updating. Putting in the extra effort to prepare your home makes it more marketable. Not only can you ask for a higher price, but it could also mean a faster sale.

Once everything is prepped, it’s time to price your home and list it on the market. After your home is listed, your real estate agent can schedule showings and greet potential buyers when they visit the property.

Although the average home sits on the market for about 54 days before going under contract, it could take more time or less before you accept an offer. The days on market can also depend on when you list your home. Research shows that November, December, January and February are the slowest months throughout the year and may even be less profitable.

After an offer is received, the response time may depend on the contract. Some contracts set offer time limits – 24, 48 or 72 hours – to dictate how long each party has to respond. Once it expires, the contract is void and a new offer must be submitted.

If there’s no contractual time limit, most agents, buyers and sellers follow common courtesy to respond within a few days after receiving an offer or counteroffer.

After accepting an offer, the buyer’s mortgage lender may require an appraisal of the property to determine the fair market value. How long the appraisal process takes depends on the complexity of the appraisal as well as the appraiser’s schedule and workload. This can take anywhere from a few days to a few weeks.

An inspection may also be required before closing and usually takes place within seven to 10 days after an offer is accepted. This typically takes a few hours and then a day or two to write the report; however, this also depends on the size and condition of the property.

If the contract contains an appraisal or inspection contingency, the potential buyer can negotiate repairs or walk away from the deal if there are any problems.

According to the National Association of Realtors’ February 2025 Realtors Confidence Index Survey, 13% of contracts had a delayed settlement within the past three months. Of those delayed contracts, 7% were delayed due to appraisal issues.

At closing, the buyer and seller will be able to review and sign the closing documents. Redfin estimates that the median number of days to close on a home after going under contract was a little over 24 days. However, the length of time it takes to get to the closing table depends on the buyer’s mortgage lender, loan type and the current housing market.

Source: realestate.usnews.com ~ By: Josephine Nesbit ~ Image: Canva Pro

Before you go all-in with your money, consider these caveats for buying a home with cash.

If you have enough money saved and the purchase won’t drain your savings, a cash purchase could be a good idea.

Key Takeaways:

If high interest rates have you dreaming about buying a house with cash, you aren’t alone. Although this is a growing trend, most people still finance their homes. According to the National Association of Realtors’ 2024 Profile of Home Buyers and Sellers, 26% of homeowners paid for their home in cash last year, an all-time high. That still means 74% of homeowners went the traditional route of taking out a mortgage.

If you think you can swing a cash purchase, should you? Here’s what you should consider when contemplating buying a house with cash.

This is obviously one of the best things about buying a house with cash. You own it, right off the bat. You have no mortgage payment. Life is good. As Lindsey Harn, a real estate agent with Christie’s International Real Estate in San Luis Obispo, California, says: “You own the home, free and clear.”

By skipping the mortgage now, you can rest assured that any increase in value on a property directly benefits you when it comes time to sell. With no mortgage to pay off, 100% of the profits from the sale go into your wallet, making it easy to purchase another home with cash or finance a larger purchase with plenty of cash on hand.

In January 2021, mortgage interest rates were 2.65%, and by October 2023, they were 7.79%. More recently, mortgage rates have hovered just under 7%.

When interest rates were historically low, borrowing was cheap. But now, “with current mortgage rates around 7%, mortgages have become less attractive,” says Jay Zigmont, a certified financial planner and CEO of Childfree Wealth, a life and financial planning firm in Mount Juliet, Tennessee.

“If you buy a house with a mortgage and invest your cash in the market, on average you are unlikely to beat a 7% return after taxes,” Zigmont says. He says homeowners who can skip a mortgage are essentially getting “a risk-free, tax-free return of the interest.”

He adds: “If I could invest my money and get a guaranteed 7% tax-free return, I’d do that all day.”

It’s also important to remember that by financing, you take on additional costs with loan origination fees and the interest paid over time, so the net cost of buying your home is less when paid for in cash.

By paying cash, you won’t have to make monthly payments to a lender, and when the house increases in value, that directly boosts your personal wealth.

Especially if you’re looking to buy an in-demand house getting a lot of interest, an all-cash offer can provide the needed leg up to get the seller to consider your offer more seriously than others. You may not even be the highest bidder, but the seller knows a cash offer will make the closing process easier.

“I’ve had sellers take cash offers over higher financed offers because, for them, it meant a guaranteed, problem-free closing,” says Brett Johnson, a real estate investor, licensed real estate agent and owner of New Era Home Buyers in Denver.

Generally, if you’re competing against another buyer, an all-cash offer puts you in a stronger position to negotiate, Johnson says. “Cash offers are appealing for sellers because they remove financing risk and provide more certainty of close,” he says.

Harn agrees. “It’s typically considered an easier transaction, so if you are competing with multiple offers, the seller may be more likely to take your cash offer as a sure thing, versus an offer contingent upon the buyer obtaining a loan and getting funding,” she says.

Part of the attractiveness of your all-cash offer is the elimination of the waiting period often imposed by mortgage lenders, filled with due diligence and underwriting to receive and approve the loan.

With a cash offer, you have the freedom to choose which aspects of the due diligence process are most important, rather than those that are required by a lender. For example, you could choose to forgo an appraisal while still having the inspection done.

While your speedier homebuyer timeline can be a powerful tool in negotiations for a purchase, don’t get carried away by neglecting aspects of due diligence that could reveal serious problems with the property in question.

“You can usually close sooner,” says Rose Krieger, a Spokane, Washington-based senior home loan specialist with Churchill Mortgage. “Instead of following the schedule set by a lender, items like the home inspection and appraisal can be completed at your discretion.”

You’re doing this on your own timetable and not a lender’s. That can smooth the process for you and the seller.

In some areas of the country that have been battered by climate change, you may find homes for sale that are uninsurable, Zigmont says. “If they are uninsurable because of previous claims, the only option is to buy it with cash. We are likely to see an increase in uninsurable homes in areas like Florida and California,” Zigmont says.

Whether you really want to pay cash for a house you can’t insure, however, is something to consider.

It may sound freeing to hear you don’t have to get your house appraised or looked over by a home inspector or get homeowners insurance, but that doesn’t mean you shouldn’t do those things.

“While a home inspection and appraisal are not necessary with a cash purchase, it is still recommended to have both of them done,” Krieger says. She also says cash buyers need to have a full picture of the true value of the home and any issues you might inherit.

“The biggest mistake cash buyers make is assuming they don’t need due diligence,” Johnson says. “Just because there are no lender requirements, don’t forgo property inspections or title research. I’ve witnessed buyers rush into deals without checking liens, zoning issues or structural problems, only to face costly surprises later.”

“Another mistake individuals make is putting too much equity into a house and not retaining enough liquidity,” Johnson says. “Real estate isn’t liquid, and I’ve seen investors who regretted not retaining enough working capital for when unexpected expenses came up.”

It’s not wise to purchase a home with cash if you have just enough to pay for it. It’s a good idea to maintain an emergency fund that will sustain you for at least a few months if you were to lose your income – covering things like car maintenance, unexpected medical costs and your regular grocery and utility costs for up to six months. You’ll also want to have cash on hand for any number of unexpected house needs, from a new roof to a furnace that’s on its last legs.

“While owning a home free and clear is great, if you have to withdraw from your retirement or sell stocks and pay taxes, getting a small loan may be better than creating a tax implication for yourself,” Harn says.

In general, after you pay for a house, you need to think about a few other future expenses that may be on the agenda:

It depends. Everybody’s financial situation is different. But if you have enough money saved to purchase a house outright and the purchase won’t drain your savings, a cash purchase could be a good idea. It may be worth your time to schedule a meeting with a financial advisor to help you run through your own personal pros and cons.

As Johnson puts it, “A cash purchase can be a wonderful tool, but use the same amount of caution on a cash purchase as on a purchase with financing.”

Source: realestate.usnews.com ~ By: Geoff Williams ~ Image: Canva Pro

Nestled in a highly desirable neighborhood near parks and top-rated schools, this stunning home has been lovingly cared for by its original owners for over 26 years. Spanning over 2, 200 square feet, the beautifully designed floor plan offers both space and functionality. As you enter, you’ll be greeted by an abundance of natural light pouring through exquisite stained glass windows in the entry room. The home is move-in ready, and you’ll immediately notice the pride of ownership throughout. Thoughtful updates in key areas ensure modern convenience while preserving its timeless charm. The backyard is the perfect size for relaxation or entertaining, and the addition of a half garage shop offers endless possibilities.

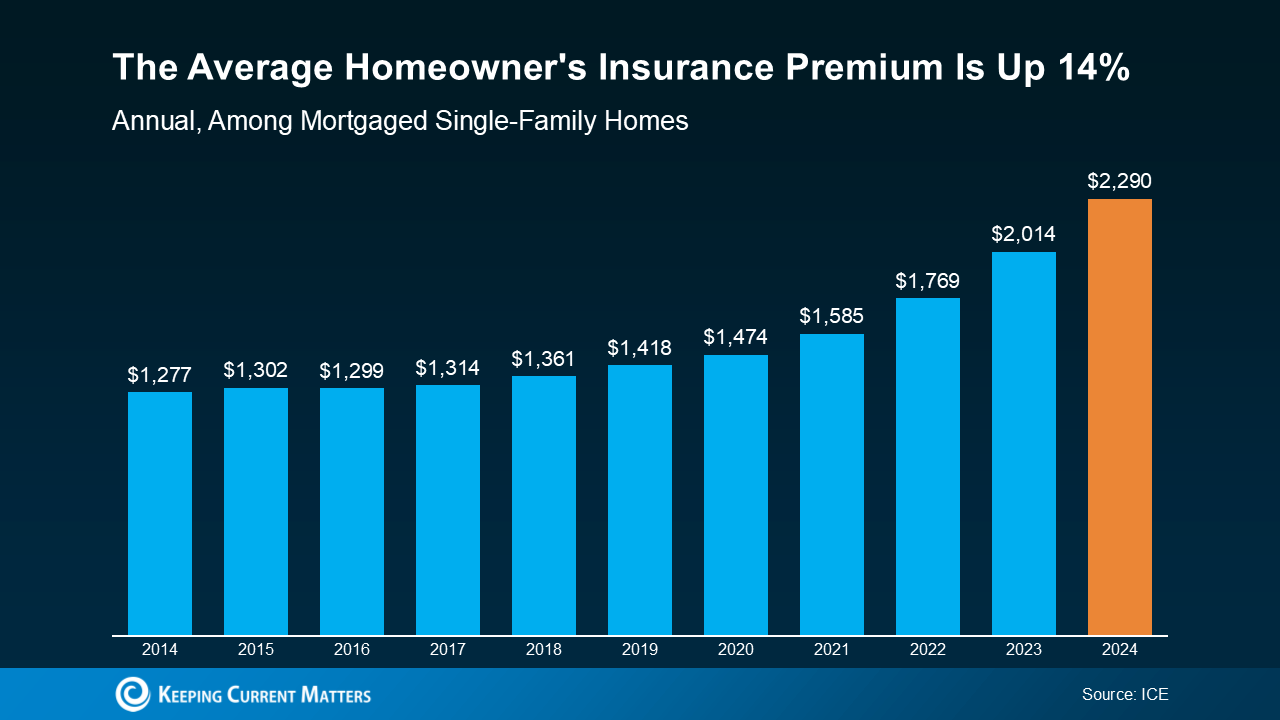

Homeowner’s insurance is a must-have to protect what’s probably your biggest investment – your home. And while you never want to think about worst-case scenarios, the right coverage is basically your safety net if something goes wrong. Here’s how it helps you.

In the simplest sense, it gives you peace of mind. Knowing you have protection against unexpected events helps you worry less. And with such a big purchase, having that reassurance is a big deal.

And while your first insurance payment will be wrapped into your closing costs, you’ll want this to be a part of your budget beyond closing day too. That’s because it’s a recurring expense you’ll have once you get the keys to your home.

Here’s what you need to know to help you budget for this important part of homeownership today.

In recent years, insurance costs have been climbing. According to Insurance.com, there are four big reasons behind the jump in premiums:

Basically, disasters are happening more often, repairs cost more, and insurers have to adjust their rates to keep up. Data from ICE Mortgage Technology helps paint the picture of how the average yearly premium has climbed over the last decade (see graph below):

Homeowner’s insurance is a must to protect your home and your investment. But with costs rising, you’ll want to do your homework to balance the best coverage you can get at the best price possible.

Homeowner’s insurance rates vary widely based on location, provider, and coverage. Shop around and compare quotes before settling on a policy. And don’t forget to ask about discounts. Things like security systems or bundling with auto insurance could help lower your insurance costs.

When you’re planning to buy a home, it’s important to look beyond just your mortgage payment. You’ll also want to budget for your homeowner’s insurance policy. It gives you a lot of protection against the unexpected. And while it’s true those costs are rising, there are things you can do to try to get the best price possible.

Source: keepingcurrentmatters.com

Welcome to 626 Sunnybrook Circle! This charming townhome offers convenience and peaceful living in a well-maintained Planned Unit Development (PUD). Located across from CSU Stanislaus, you’re just minutes from dining, shopping, and schools in a quiet, established neighborhood. The bright living area opens to a private, gated patio with access to a grassy common space. The kitchen features updated appliances, cabinets, granite and including a refrigerator. Upstairs, you’ll find two spacious bedrooms, a remodeled full bathroom, and a laundry are. A half-bath is conveniently located downstairs. The Carpet is Brand New! Unlike many townhomes, this property includes a full-size two-car garage. The community offers beautifully landscaped grounds, tree-lined streets, a swimming pool, and a clubhouse. Don’t miss this move-in-ready home in a prime location!

A pre-listing home inspection is the same as a standard home inspection except that the seller pays for it before listing their home on the market.

Jennifer Smeltzer, a top-performing real estate agent in Jackson County, Missouri, advises sellers to complete the pre-listing inspection no sooner than two months before listing their property. This way, buyers trust that the inspection findings are indicative of the home’s current condition.

During a pre-listing home inspection, a certified home inspector will assess the property, noting the condition of major structural components and features.

According to the American Society of Home Inspectors, a home inspection checks a home’s:

The inspector will determine whether there are any issues with these features, looking for signs of damage like leaks, cracks, faulty wiring, and code violations. It’s important to keep in mind that most home inspections do not evaluate the condition of the paint, wallpaper, and other finishes.

How can a pre-listing home inspection benefit your sale?

The main advantage of conducting a pre-listing home inspection is it allows you to identify issues and complete repairs before a buyer is involved. Let’s take a look at how this and other benefits can accelerate the home sale process.

Get ahead of repairs

Common home repairs can take weeks to months to book and complete. A pre-listing home inspection gives you time to compare contractors and tackle repairs without the pressure of a buyer threatening to walk away from the sale.

Be aware that state laws mandate that sellers need to disclose known property issues to buyers. You’ll need to disclose any pre-listing inspection findings that you choose not to fix.

Reduce points of negotiation

Buyers often use home inspection findings to negotiate for a lower sale price or repair credits. For example, say an inspection reveals a major crack in the foundation that would cost $4,000 to repair. The buyer may ask that you either complete the repair or give them a $4,000 repair credit at closing. If the buyer included an inspection contingency in their offer, they can leave the deal with their earnest money intact if you don’t agree to their request.

With a pre-listing home inspection, you beat the buyer to the punch by completing (or at least acknowledging) these repairs ahead of time. Bypassing the usual inspection negotiations, which often last one to three days, can get you to closing faster.

As Smeltzer puts it:

Whether we fix those issues or we don’t, at least we know that they are there. Knowing this can help us determine a price point and stand confidently with that price during negotiations with buyers

- Determine an effective price point

Whether you tend to all, some, or none of the pre-listing home inspection findings, knowing your property’s condition can help set a strategic price. For instance, you might disclose that the roof needs repairing and share that the listing price reflects this discount. On the flip side, if you know your property is in perfect condition, you can price and market it as a turnkey home to encourage higher offers.

Encourage stronger offers

If you’ve conducted a pre-listing home inspection, you can market your home as “pre-inspected” and show buyers the inspection report along with relevant repair invoices. This documentation gives potential buyers the confidence to put in a higher offer because they know that there won’t be any surprise repair costs down the line.

“In my market, a pre-listing home inspection isn’t done a whole lot of the time, but it’s an added value … It’s definitely something that a buyer would want to see,” notes Smeltzer.

If a buyer is torn between offering on your home or another, the pre-inspection bonus may just serve as the tiebreaker they need.

Prepare for an FHA appraisal

If a buyer is backed by a Federal Housing Administration (FHA) loan, your home will need to pass an FHA home appraisal. This intensive appraisal process functions similarly to a home inspection as the FHA appraiser assesses the property’s overall condition.

For the buyer’s loan to close, the seller must attend to any repairs “necessary to maintain the safety, security, and soundness of the Property, preserve the continued marketability of the property, and protect the health and safety of the occupants.”

The entire list of necessary repairs is extensive and includes the following issues:

How much do pre-listing home inspections cost?

In general, an inspection for an average-sized residential property takes just a few hours to complete and costs on average between $300 and $425. According to HomeAdvisor, many home inspectors charge a flat fee for homes up to 2,000 square feet and charge per square foot thereafter.

Note that even with a pre-listing home inspection completed, your buyer may still order their own inspection before purchasing the property. In this case, it’s customary for the buyer to pay for the inspection.

How to determine if a pre-listing home inspection is right for you

While a pre-listing home inspection can certainly speed things up, it isn’t always the right choice. Smeltzer tells us that she recommends pre-listing home inspections on a case-by-case basis. “A lot of times, a seller may not want to pay for the additional expense when they know the buyer is going to go ahead and do their own inspection, as well.”

To help you figure out whether or not a pre-listing home inspection is right for you, consider the following:

You should seriously consider a pre-listing home inspection if:

You may want to skip the pre-listing home inspection if:

If you are still unsure of whether or not you want to pay for a pre-listing home inspection, consult your real estate agent. An experienced real estate agent knows their local market well and can advise if a pre-listing home inspection can benefit your sale.

Source: homelight.com ~ By: Matthew Stalcup & Kelsey Morrison ~ Image: Canva Pro