Here’s a piece of good news for rate-weary buyers: Relief is on the way. After months of turmoil, the housing market should be slightly calmer in 2024.

Although the factors that tanked affordability in 2023 — mainly high mortgage rates and lack of inventory — will still be at play in 2024, no one expects conditions to get any worse for buyers and sellers. In fact, many housing experts believe the new year will be a turning point for real estate: They say home sales should (somewhat) rebound, mortgage rates and prices should move lower, and more sellers will list their homes.

To be sure, these improvements will be gradual, and “housing affordability is still going to be the No. 1 issue for homebuyers,” says Danielle Hale, chief economist at Realtor.com. But slightly lower mortgage rates and prices will help lower the costs of homeownership.

What else can we expect from the 2024 housing market? Here’s what experts predict will happen with mortgage rates, inventory, home prices, and sales in the near future.

Mortgage rates will decrease

Mortgage rates were one of the main obstacles for homebuyers in 2023. After starting the year on a downswing, they quickly turned tail and headed up to two-decade highs, even flirting with 8% at one point.

But rates have eased lower in the last two months. A slowing economy, weakening labor market, and steady improvement in the battle against inflation led the Federal Reserve to hold the federal funds rate steady over the past few months and signal the possibility of rate cuts in 2024.

As a result, 10-year Treasury yields and the mortgage rates that follow their movement have dropped. Freddie Mac’s 30-year fixed-rate loan averaged below 7% for the first time since mid-August, and all the experts Money spoke to agree the downward trend will continue in the new year (although it’s not guaranteed).

However, don’t expect a dramatic drop into the 3% or 4% range. As with home sales, there’s a wide range of predictions for how low rates will go.

On the higher end, listing site Zillow expects interest rates to stay between 7% and 7.5% throughout the year. The National Association of Realtors is a little more optimistic, expecting rates to average below 7% by the start of the upcoming spring buying season and end the year at around 6.3%. In contrast, Realtor.com expects rates to end 2024 averaging 6.5%. With mortgage rates averaging 6.61% and trending lower at the end of December, it’s looking good for rates to stay below 7% this year.

Inventory will increase

Last year, sellers were loath to list their homes because they didn’t want to give up the low mortgage rates they’d previously locked in. As a result, there weren’t a lot of homes to choose from in 2023.

Thankfully, buyers can expect to see some improvement in the number of homes up for sale in 2024. Overall, inventory could increase by as much as 30% compared to last year, according to Lawrence Yun, chief economist at NAR, with some markets seeing even faster growth.

Skylar Olsen, chief economist at Zillow, says she has noticed in recent research that some homeowners who bought when rates were in the 5% and 6% range have readjusted their expectations around how low rates will go. They “are much less sensitive” to the rate-lock effect, Olsen says, adding that the rate homeowners consider “low enough” to prompt them to sell is increasing.

Home prices will likely stay flat

While there should be some improvement in housing supply and mortgage rates, the dynamics that have kept home prices high will continue.

Inventory is still well below demand. Before the pandemic, the number of active listings on the market averaged over 1 million homes, according to the St. Louis Fed. At the end of November, there were 754,846.

What does this mean for the market? Buyers are competing for fewer available homes, keeping upward pressure on home prices. So, on a national level, prices aren’t going to plummet unless we get a sudden and large influx of listings. Most experts forecast home prices will remain flat or decrease by about 1% in 2024.

That doesn’t mean there won’t be some markets where home prices majorly decline. There are currently a handful of cities where prices have decreased significantly, such as San Francisco and Las Vegas, and there’s a probability more cities will see considerably lower prices — just not on a level that could jeopardize the housing market as a whole.

Home sales will increase

Most housing analysts expect sales to improve this year thanks to improving overall market conditions. But not everyone agrees just how much better it will be.

The most conservative estimate for home sales comes from Realtor.com, which forecasts existing home sales to increase by 0.1% year-over-year, or a jump of about 4 million homes sold. At the opposite end of the spectrum is NAR, which is forecasting sales to increase by 13.5% compared to 2023.

It all goes back to — you guessed it — the hope that mortgage rates will continue to edge lower, which Yun says “will bring out more buyers and may even nudge some sellers to list their homes.”

Source: money.com ~ By: Leslie Cook ~ Image: Canva Pro

Homeowners insurance covers damage to your home from fire, heavy wind, and other disasters.

Nerdy takeaways

Homeowners insurance provides coverage in case a disaster damages your home or personal belongings.

It can also pay out if you’re held responsible for an accident or injury.

Home insurance generally covers damage due to fire, wind or snow, but it won’t cover floods or earthquakes.

Your home is more than just a roof over your head. It may be your most valuable asset — and one you likely can’t afford to replace out of pocket if disaster strikes. That’s why protecting your place with the right homeowner’s insurance is important.

What does homeowners insurance cover?

Homeowners insurance covers your house and belongings in case of events such as fires, hail, tornadoes, and burst pipes. If one of these scenarios damages your home, your policy can pay to repair it. Homeowners insurance can also reimburse you for theft or vandalism of your belongings.

But a homeowners policy doesn’t just cover your house and your stuff. It can also pay to defend you from lawsuits or cover medical bills for someone who gets hurt on your property. And if you can’t live at home after a covered disaster, your homeowner’s policy could pick up the tab for a hotel or rental apartment.

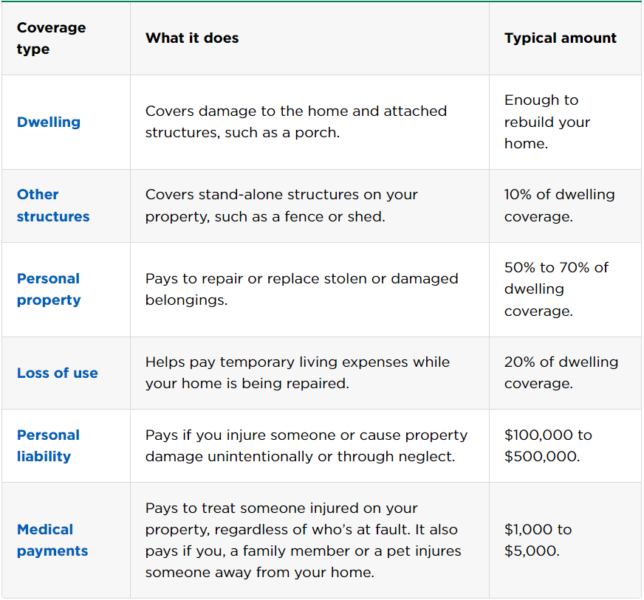

The 6 standard types of home insurance coverage

Standard homeowners insurance policies generally include these six types of coverage:

Dwelling coverage

Dwelling coverage covers the structure of your home, including the walls, floors, windows, and roof. Built-in appliances, such as furnaces, are typically included in your dwelling coverage. An attached garage, porch, or deck would fall under your dwelling coverage, too.

Which events are covered: Most homeowner’s policies cover your dwelling for any cause of damage that isn’t specifically excluded. According to the Insurance Information Institute, some of the most common causes of homeowners insurance claims include wind, hail, freezing, fire, and lightning.

How it works: A severe thunderstorm uproots a tree that falls onto your home, crushing part of the roof and attic. You’d pay your share of the repair cost — known as the homeowners insurance deductible — and then the insurer would pay the rest, up to your dwelling coverage limit.

Other structures coverage

Just like it sounds, other structures coverage provides insurance for structures on your property that aren’t attached to your house. That could include a shed, fence, or detached garage.

Which events are covered: As with dwelling coverage, most homeowners insurance policies cover other structures for any event that isn’t specifically excluded. That means you’d likely have coverage for fire, wind, hail, and snow, among other issues.

How it works: Part of your fence collapses under the weight of heavy snow. The insurance company would pay to repair it, minus your deductible.

Personal property coverage

Personal property refers to your personal belongings — like clothes, furniture, electronic devices, and appliances that aren’t built in. Most homeowners’ policies cover these items anywhere, not just inside your house. So if someone steals your bike from outside a store, it’ll likely be covered (minus your deductible).

Which events are covered: In most homeowner’s policies, personal property coverage works differently than dwelling and other structures coverage. Instead of covering your belongings for anything that isn’t specifically excluded, homeowner’s policies often cover only disasters that are listed.

These events, typically called “perils” in your policy, tend to include:

Fire or lightning.

Smoke.

Windstorms and hail.

Explosions.

Theft.

Vandalism.

Weight of ice, snow, and sleet.

Sudden damage from a power surge.

Volcanic eruptions.

Falling objects.

Water overflow or discharge from household systems like plumbing, air conditioning, and appliances.

Freezing of those same household systems.

Sudden tearing, cracking, or bulging of a hot water system, steam system, air conditioning, or fire protective system.

Riots.

Damage from aircraft or vehicles.

How it works: A pipe bursts on a frigid winter night, sending water cascading into your kitchen and dining room. Although dwelling coverage would pay for damage to built-in items such as cabinets, personal property coverage would take care of ruined furniture, minus your deductible.

Loss of use coverage

Sometimes called “additional living expenses,” the loss of use a section of your homeowner’s policy can come in handy if your home is too damaged to live in. Loss of use coverage may pay for hotel stays, restaurant meals, or other expenses associated with living somewhere else if your home is uninhabitable after a disaster your policy covers.

Which events are covered: As long as your home is undergoing repairs for a covered claim, you’ll likely be eligible for loss of use coverage. But if your home’s damage is from a disaster that isn’t covered — such as a flood — your insurer won’t pay your additional living expenses, either.

How it works: After a kitchen fire spreads to your living room, your home is out of commission for a few months while contractors make repairs. Your insurance company would pay for you and your family to rent a similarly sized house nearby.

Liability coverage

Personal liability coverage offers financial help if you’re responsible for injuring someone or damaging their property. Coverage generally extends to anyone in your household, including pets — so if your dog bites someone at the park, you may have coverage. (See Does Homeowners Insurance Cover Dog Bites? for more information.)

Which events are covered: Liability insurance covers bodily injury and property damage to others, with some exceptions. For instance, your policy won’t cover criminal acts or harm you cause on purpose. Nor will it pay for injuries or damage from a car accident (your liability car insurance would cover those).

How it works: A delivery person slips on your icy sidewalk before you can salt it. He breaks his wrist in the fall and sues you for medical bills and lost wages. Your liability coverage could pay your legal fees, plus any damages you’re responsible for in the lawsuit, up to your policy limit.

Medical payments coverage

Like liability coverage, medical payments coverage pays if you cause physical injury to someone outside your household. However, you don’t need to be found at fault for medical payment coverage to pay out.

Which events are covered: You could tap your medical payments coverage if someone suffers a minor injury on your property or you cause harm to someone outside your home. Similar restrictions apply to liability and medical payments, with no coverage for intentional acts or car accidents, among other exclusions.

How it works: Your dog bites the hand of a visiting friend. There’s no serious harm, but your medical payments insurance covers the cost of their trip to urgent care for stitches.

What homeowners insurance won’t cover

Even the broadest homeowners insurance policy won’t cover everything that could go wrong with your home. For example, you can’t intentionally damage your house and then expect your insurer to pay for it. Policies also typically exclude damage from other causes such as:

Flooding from external sources like heavy rainfall or storm surges.

Drain and sewer backups.

Earthquakes, landslides, and sinkholes.

Infestations by birds, vermin, fungus, or mold.

Wear and tear or neglect.

Nuclear hazard.

Government action, including war.

Power failure.

However, you can buy separate coverage for some of these risks. Flood insurance and earthquake insurance are available separately, and in hurricane-prone states, you may need or want windstorm insurance.

Expand your coverage with endorsements

Talk to your insurer if you have concerns about problems your policy doesn’t cover. In many cases, you can add endorsements — which usually cost extra — that offer more coverage.

Below are a few of the most common home insurance endorsements. Note that availability may vary by state and company.

Scheduled personal property covers a specific valuable item such as a ring or musical instrument. You may need an appraisal — a document that states the value of the item — to get this coverage.

Ordinance or law coverage pays to bring your home up to current building codes during repairs or rebuilding.

Water backup coverage pays for damage due to backed-up sewer lines, drains, or sump pumps.

Equipment breakdown coverage pays for heating, ventilation, and air conditioning, or HVAC, systems, and large appliances if they stop working for reasons other than normal wear and tear.

Service line protection pays for damage to water, electricity, or other utility lines that you’re responsible for.

Identity fraud coverage pays expenses associated with identity theft such as lost wages and legal fees.

Does homeowners insurance cover …?

This table shows common problems and whether your homeowner’s insurance policy will cover them.

If a covered event knocks a tree onto your home, your policy will probably pay to remove it. But if the tree simply falls on your lawn, you’re on your own. Learn more about home insurance and tree removal.

Fire

Usually.

Fire is one of the standard perils most homeowners insurance policies cover. Learn about home insurance and wildfires.

HVAC problems

Maybe.

If a covered event such as a windstorm damages your heating or cooling system, your homeowner’s policy would likely pay to repair it. Adding an equipment breakdown endorsement to your policy could give you additional coverage for mechanical failures. However, homeowners insurance won’t pay for normal wear and tear. Learn more about homeowners insurance and AC units.

Lost jewelry

Usually not.

A standard homeowners insurance policy covers jewelry only for theft, fire or other named events, not for accidental loss. That’s why it’s a good idea to add broader coverage for valuable jewelry. Learn more about jewelry insurance.

Mold

Maybe.

It depends on the cause of the mold. Most insurers will cover mold only if it’s caused by a covered problem such as a burst pipe. Learn more about homeowners insurance and mold.

Plumbing

Maybe.

Damage from sudden, accidental leaks may be covered, but slow leaks that develop over time generally won’t be. (The latter are considered a maintenance issue.) See Does Homeowners Insurance Cover Plumbing Problems?

Roof leaks

Maybe.

It depends on why your roof is leaking. Insurance typically covers damage due to a sudden, accidental event such as hail or wind, but it won’t cover simple wear and tear. Learn more about homeowners insurance and roof leaks.

Termite damage

Usually not.

Insurance companies generally consider dealing with infestations to be a part of regular home maintenance, which they don’t cover. Learn more about homeowners insurance and termite damage.

Water damage

Maybe.

It depends on the type of water damage. Most home insurance policies won’t cover floods, for example. They won’t cover damage from a backed-up drain or sewer unless you’ve paid for that endorsement. But if a pipe freezes and bursts, your insurer will typically pay for the resulting damage. To learn more, see Does Homeowners Insurance Cover Water Damage?

Types of homeowners insurance policies

Homeowners insurance comes in several types, called “policy forms.” Some types have more expansive coverage than others, so it’s worthwhile to know the difference. Note that different insurance companies may have different names for these policies.

Most popular: HO-3 insurance

HO-3 insurance policies, also called “special form,” are the most common. If you have a mortgage, your lender is likely to require at least this level of coverage.

HO-3 insurance policies generally cover damage to your home from any cause except those the policy specifically excludes, such as an earthquake or a flood. However, where it concerns your belongings, HO-3 insurance typically covers only damage from the perils listed in your policy.

Broadest coverage: HO-5 insurance

An HO-5 insurance policy offers the most extensive homeowners coverage. It pays for damage to your home and belongings from all causes except those the policy excludes. It’s typically available only for well-maintained homes in low-risk areas, and not all insurers offer it.

Limited coverage: HO-1 and HO-2 insurance

Much less popular are HO-1 and HO-2 homeowners insurance, which pay only for damage caused by events listed in the policy.

Other policy types include HO-4 insurance for renters, HO-6 for condo owners, HO-7 for mobile homes, and HO-8 — a rarely used type that provides limited coverage for older homes.

How homeowners insurance works

If your home is destroyed, your homeowner’s insurance company isn’t likely to simply write you a check for the amount listed on your policy. First, you’ll have to file a claim, documenting the damage. And your payout could vary depending on your coverage and deductibles.

Replacement cost vs. actual cash value

One key factor in your payout is whether your coverage will pay whatever it takes to rebuild your home, even if that cost is above your policy limits. This situation may arise, for instance, if construction costs have increased in your area while your coverage limits haven’t changed. Here’s a rundown of several options you may encounter.

Actual cash value coverage pays the cost to repair or replace your damaged property, minus a depreciation deduction. Most policies don’t use this method for the house, but it’s common for personal belongings. For items that are several years old, this means you’ll probably get only a fraction of what it would cost to buy new ones. Learn more about actual cash value coverage.

Functional replacement cost coverage pays to fix your home with materials that are similar but possibly cheaper. For example, your contractor could replace damaged plaster walls with less expensive drywall.

Replacement cost coverage pays to repair your home with materials of “like kind and quality,” so plaster walls can be replaced with plaster. However, the payout won’t go above your policy’s dwelling coverage limits.

Some policies offer replacement cost coverage for personal items. This means the insurer would pay to replace your old belongings with new ones, with no deduction for depreciation. If this feature is important to you, check the policy details before you buy. It’s a common option, but you typically need to pay more for it. Learn more about replacement cost coverage.

Extended replacement cost coverage will pay more than the face value of your dwelling coverage, up to a specified limit, if that’s what it takes to fix your home. The limit can be a dollar amount or a percentage, such as 25% above your dwelling coverage amount. This gives you a cushion if rebuilding is more expensive than you expected.

Guaranteed replacement cost coverage pays the full cost to repair or replace your home after a covered loss, even if it goes above your policy limits. Not all insurance companies offer this level of coverage.

Homeowners insurance deductibles

Homeowners’ policies typically include a deductible — the amount you must cover before your insurer starts paying. The deductible can be:

A flat dollar amount, such as $500 or $1,000.

A percentage, such as 1% or 2% of the home’s insured value.

When you receive a claim check, your insurer subtracts your deductible amount. Say you have a $1,000 deductible and your insurer approves a claim for $10,000 in repairs. The insurer would pay $9,000, and you would be responsible for $1,000.

Be aware that some policies include separate — and often higher — deductibles for specific types of claims such as damage from wind, hail, hurricanes or earthquakes. For example, a policy might have a $1,000 deductible for most losses but a 10% deductible for optional earthquake coverage. This means if an earthquake damages a home with $300,000 worth of dwelling coverage, the deductible would be $30,000.

Liability claims generally don’t have a deductible.

There are plenty of perks to owning your own home rather than renting. You can knock down walls if you want to, you can install a professional home theater system, or you can paint the walls with purple polka dots if you like. But there are other benefits—the financial kind.

If you rented in the past, all of your money went to a landlord, and none of it came back to you as a tax deduction. That changes if you’re a homeowner.

Whether you buy a mobile home, townhouse, condominium, cooperative apartment, or single-family home, several tax breaks can save you money at tax time.

The downside is that your taxes will get more complicated. You can’t just plug your W-2 information into Form 1040 and finish your taxes in 10 minutes. As a homeowner, you can take advantage of itemizing, which can save you a lot of money.

KEY TAKEAWAYS

The Internal Revenue Service (IRS) provides several tax breaks to make homeownership more affordable.

Common tax deductions include those for mortgage interest, mortgage points, and private mortgage insurance (PMI).

To claim the deductions, you have to itemize your taxes rather than taking the standard deduction.

Tax credits are available for qualified first-time homebuyers and homeowners who invest in energy improvements like solar panels and energy-efficient windows.1

The standard deduction for the 2024 tax year is $29,200 for couples filing jointly, and $1,460 for singles. That’s up from $27,700 for couples and $13,850 for singles in 2023.2 You might do a quick calculation of your deductions and see if the standard deduction saves you more.

Tax Credits vs. Tax Deductions

In the tax world, there are deductions, and there are credits. Credits are better.

A credit is directly subtracted from your tax bill. If you get a $1,000 tax credit, your total tax amount due will decrease by $1,000.

A tax deduction reduces your adjusted gross income (AGI), which reduces the amount of taxes you owe. For example, if you’re in the 24% tax bracket, your tax liability will be reduced by 24% of the total claimed deduction. If you claim a $1,000 deduction, your tax liability will drop by $240 ($1,000 × 24%).

Tax Deductions for Homeowners

Most of the favorable tax treatment that comes from owning a home is in the form of deductions. Here are the most common deductions:

Mortgage Interest Deduction

You can deduct your home mortgage interest on the first $750,000 ($375,000 if married filing separately) of mortgage debt. The old limit—$1 million ($500,000 if married filing separately)—applies if you bought your home before Dec. 16, 2017.3

You can’t deduct home mortgage interest unless you itemize deductions on Schedule A Form 1040 or 1040-SR. You can deduct mortgage interest on a second home as long as the mortgage satisfies the same requirements for deductible interest as on your primary residence.4

In January, after the end of the tax year, your lender will send you Internal Revenue Service (IRS) Form 1098, detailing the amount of interest that you paid in the previous year.5

If you just bought your home, be sure to include any interest that you paid as part of your closing. Lenders will include interest for the partial first month of your mortgage as part of your closing. You can find it on the settlement sheet. Ask your lender or mortgage broker to point this out to you. If it’s not included on your 1098, add this to your total mortgage interest when doing your taxes.

Mortgage Points Deduction

You may have paid mortgage points to your lender as part of a new loan or refinancing. Each point that you buy generally costs 1% of the total loan and lowers your interest rate by 0.25%. For example, if you paid $300,000 for your home, each point would equal $3,000 ($300,000 × 1%).

With a 4% interest rate, for instance, that one point would lower the rate to 3.75% for the life of the loan. As long as you actually gave the lender money for these discount points, you get a deduction.

Like the mortgage interest deduction, discount points are deductible on the first $750,000 of debt.

If you refinanced your loan or took out a home equity line of credit (HELOC), you receive a deduction for points over the life of the loan. Each time you make a mortgage payment, a small percentage of the points is built into the loan. You can deduct that amount for each month that you made payments. So, if $5 of the payment was for points, and you made a year’s worth of payments, your deductible amount would be $60.40

Your lender will send you Form 1098, detailing how much you paid in mortgage interest and mortgage points. Using that information, you can claim the deduction on Schedule A of Form 1040 or 1040-SR.67

Private Mortgage Insurance (PMI)

Lenders charge private mortgage insurance (PMI) to borrowers who put down less than 20% on a conventional loan.8 PMI usually costs $30 to $70 a month for each $100,000 borrowed. Like other types of mortgage insurance, PMI protects the lender (not you) if you stop making mortgage payments.

Depending on your income and when you bought your home, you might be able to deduct your PMI payments.9

Mortgage insurance premiums are no longer deductible.10

State and Local Tax (SALT) Deduction

The state and local tax (SALT) deduction lets you deduct certain taxes paid to state and local governments if you itemize on your federal return.

The $10,000 cap applies whether you are single or married filing jointly and drops to $5,000 if you’re married filing separately.11 The deduction limit relates to the combined total deduction of state income, local income, sales, and property taxes.

You must itemize your deductions to claim the mortgage interest deduction, mortgage points deduction, and SALT deduction. You can’t claim these deductions if you take the standard deduction when filing your tax return.

If you pay your property taxes through a lender escrow account, you’ll find the amount on your 1098 form.5

Otherwise, you can look at your personal records in the form of a check or automatic transfer if you pay directly to your municipality.

Be sure to include payments that you made to the seller for any prepaid real estate taxes (you can find them on your settlement sheet).

State and local income taxes withheld from your paycheck appear on your W-2 form, which your employer(s) should send by the end of January following the tax year.1213 If you elect to deduct state and local sales taxes instead of income taxes (you can’t deduct both), you can use your actual expenses or the optional sales tax tables found in Schedule A (Form 1040).1415

Home Sale Exclusion

Chances are you won’t have to pay taxes on most of the profit that you make when you sell your home, thanks to the home sale exclusion.

If you’ve owned and lived in the home for at least two of the five years before the sale, you won’t pay taxes on the first $250,000 of profit (that is, the capital gain). The number doubles to $500,000 if you’re married filing jointly. However, at least one spouse must meet the ownership requirement, and both spouses must meet the residency requirement that they have lived in the home for two out of the previous five years.16

You might be able to meet part of the residency requirement if you had to sell your home early due to a divorce, a job change, or some other reason.

If you have a taxable gain on the sale of your main home that is greater than the exclusion, report the entire gain on Form 8949: Sales and Other Dispositions of Capital Assets.17

Short-term capital gains tax rates apply if you owned the home for less than a year. These gains are taxed at your ordinary income tax rate, which will be somewhere between 10% and 37% depending on your income for the year. 18

Long-term capital gains tax rates apply if you owned the home for more than a year. The rate is 0%, 15%, or 20%, depending on your filing status and income.19

Tax Credits

You might be eligible for a mortgage credit if you were issued a qualified mortgage credit certificate by a state or local governmental unit or agency under a qualified mortgage credit certificate program.20

Also, check energy.gov to find out whether your state offers tax credits, rebates, and other incentives for energy-efficient improvements to your home.

Which Expenses Can I Itemize?

Homeowners can generally deduct home mortgage interest, home equity loan or home equity line of credit (HELOC) interest, mortgage points, private mortgage insurance (PMI), and state and local tax (SALT) deductions.

Whether or not you’re a homeowner, you may be able to deduct charitable donations, casualty and theft losses, some gambling losses, unreimbursed medical and dental expenses, and long-term care premiums.

You itemize your deductions on Schedule A Form 1040.

Who Should Itemize Deductions?

All taxpayers have the option of taking the standard deduction or itemizing deductions. You can take whichever option saves you the most.

The standard deduction for the 2024 tax year is $29,200 for couples filing jointly and $1,460 for singles. For the 2023 tax year, it’s $27,700 for couples and $13,850 for singles.2

Note that these numbers are double the standard deduction amounts available before 2018 when the tax code got an overhaul. You might do a quick calculation of your deductions and see if the standard deduction saves you more.

What Are the Standard Deduction Amounts for 2023?

For the 2023 tax year, the standard deduction is $13,850 for single people or married couples filing separately, $20,800 for heads of household, and $27,700 for married filing jointly couples.

For the 2024 tax year, the deduction is $14,600 for single people or married couples filing separately, $21,900 for heads of household, and $29,200 for couples who are married filing jointly.18

The Bottom Line

Let’s keep this in perspective: If you’re in the 24% tax bracket, you’re still paying nearly 75% of your mortgage interest without any deductions.

Don’t fall into the trap of thinking that paying interest is beneficial because it reduces your taxes. In many cases, paying off your home as quickly as possible is the best financial move, particularly with the much larger standard deduction now in effect.

Nobody buys or sells a home in the winter, right? Well, if you checked the numbers, you’d find that plenty of homes are sold during the coldest months of the year. From December 2022 to February 2023, nearly 800,000 homes sold in the U.S. That’s a lot of houses!

In other words, the number of homes bought and sold during the winter is nothing to sneeze at. Plus, since most buyers search for homes online these days, it’s not like outdoor temperatures are keeping potential buyers from looking around.

If you’re wondering whether you should put off buying or selling a home until spring, there’s no need to wait. In fact, there are several advantages to buying or selling while Jack Frost is nipping at your nose. Let’s look at some of the biggest ones and go over some tips that’ll get you moving in the right direction.

Tips for Selling in the Winter

Nothing says welcome home quite like the smell of a gingerbread candle and some Christmas lights—it’s easier to stage a house and make it feel like home in the wintertime!

Here are a few tips to help you set the buying mood:

Keep it simple. If you’re selling around a holiday and have decorations up, make sure they accent—not overpower—a room. Less is more.

Crank up the cozy. Light a fire in the hearth, play soft holiday music in the background, and prepare fresh-baked goods or mulled cider for guests.

Shine a light outside. Winter days get dark early. Brighten your home’s exterior with outdoor spotlights.

Take down outside decor. Nothing says “my home won’t sell” like a house with reindeer inflatables on the lawn in February.

Avoid a winter wonderland. Snow is great—unless we’re talking about outside shots of your home. Buyers want to see details of the house, not a blanket of snow. Make sure you have clear-weather photos of your home.

Remember, the nicer your home looks, the more likely it is to sell—and for more money.

Advantages of Selling Your Home in the Winter

Okay, huddle up, home sellers. Let’s unpack the perks of selling when the air gets chilly.

1. You’ll face less competition.

Come spring, more sellers will flood the market and your home will be just another fish in a great big pond. But in winter, you’ve got a limited number of sellers on the market. For example, the number of active home listings in the U.S. during 2021 and 2022 dipped during the winter and didn’t begin rebounding until the spring of the following year.2

If that pattern repeats in 2023–2024, you’ll have less competition on the market if you list your home during the winter! Buyers have fewer homes to choose from, which means you could sell your house faster.

2. Buyers often mean business.

Most folks want to curl up under a blanket next to a warm fire on a cold winter day. If a buyer is trudging around in freezing weather or breaking away from their holiday schedule to look at your home, they must be serious. That’s because many winter buyers are working against a deadline, whether it’s an expiring lease, relocation, or a contract on their current home. They may also be trying to snag some tax breaks before the end of the year.

3. People have time off during the holidays.

You may think people are less likely to see your home in the midst of their hectic holiday schedules. That can definitely be true. But keep in mind, that many people also have more time off around the holidays. That means more time for browsing their favorite home apps, dreaming about their future decor, and even scheduling home showings.

Tips for Buying in the Winter

Alright, home buyers. Now it’s your turn. Below are some tips for buying a house when the weather outside is frightful.

Don’t buy until you’re debt-free with an emergency fund. Hold off on buying a home if you haven’t paid off all your consumer debt (think credit cards, car notes, and student loans) or saved up a full emergency fund worth 3–6 months of your typical expenses. You should prioritize those financial goals first.

Save up a strong down payment. You need to make a strong down payment when you buy a home because a bigger down payment means smaller monthly payments and less debt overall. Aim for a 20% down payment since that’ll keep you from having to pay monthly private mortgage insurance fees. (A 5–10% down payment is fine if you’re a first-time home buyer, though.)

Stick to your budget. Sure, home prices might drop a bit with the temperatures. But that doesn’t mean you should justify spending any more than 25% of your monthly take-home pay on monthly housing payments. To make sure your winter home purchase is a blessing and not a curse, calculate how much house you can afford and stick to it.

Negotiate with confidence. Remember, there isn’t much competition. So, sellers will probably be willing to work with you. If the home inspection brings up some issues, don’t be afraid to ask your seller to make repairs or lower the asking price.

Advantages of Buying Your Home in the Winter

Now, here are some of the biggest advantages to buying a home in winter:

1. You’ll have less competition.

Home sellers aren’t the only ones who face less competition during the winter! As we saw earlier, home sales take a bit of a plunge during the winter. So, typically, you won’t have to deal with as many competing buyers as you would if you waited to buy in spring. This probably means you don’t have to worry as much about someone else snagging your dream home before you can submit an offer, or about getting caught in a bidding war.

It’s kind of like when someone brings in holiday treats to share with the office but most of your coworkers are out of town. You get first dibs on the best desserts!

2. You may get a better deal.

Since supply and demand for housing are both down during the winter months, you might be able to save money on your purchase! Hard to believe? Get this: The median sales price of homes sold from December 2022 to February 2023 was about $20,000 lower than homes sold from March to May 2023.

That means people who bought their homes during winter saved tens of thousands of dollars compared to those who waited to buy in the spring or summer! That might make any challenges of buying during the wintertime worthwhile.

3. You can lock in the current mortgage rate.

As you’ve probably heard, interest rates have climbed up a lot lately. Well, there’s a chance that the trend will continue moving forward since the Federal Reserve (the Fed) could raise the national interest rate again at its next meeting. So, if you’re going to use a mortgage to buy a house, locking in your rate now could save you from paying even more down the road. And if rates wind up going down over the next year or so, you can always refinance.

If you follow these tips, there’s hope you’ll find the house you want and get a good price on it this winter.

Ready to Buy or Sell Your Home in Winter?

With all these advantages on your side, hopefully buying or selling your home in the winter won’t feel so daunting. We know you’ve probably got a lot on your plate this time of year though. So, we’ve put together some resources to help you check everything off your list. For a step-by-step plan that’ll walk you through every part of the process, use our free Home Buyers Guide or Home Sellers Guide.

If you’ve ever dreamed of buying your own place, or selling your current house to upgrade, you’re no stranger to the rollercoaster of emotions changing home prices can stir up. It’s a tale of financial goals, doubts, and a dash of anxiety that many have been through.

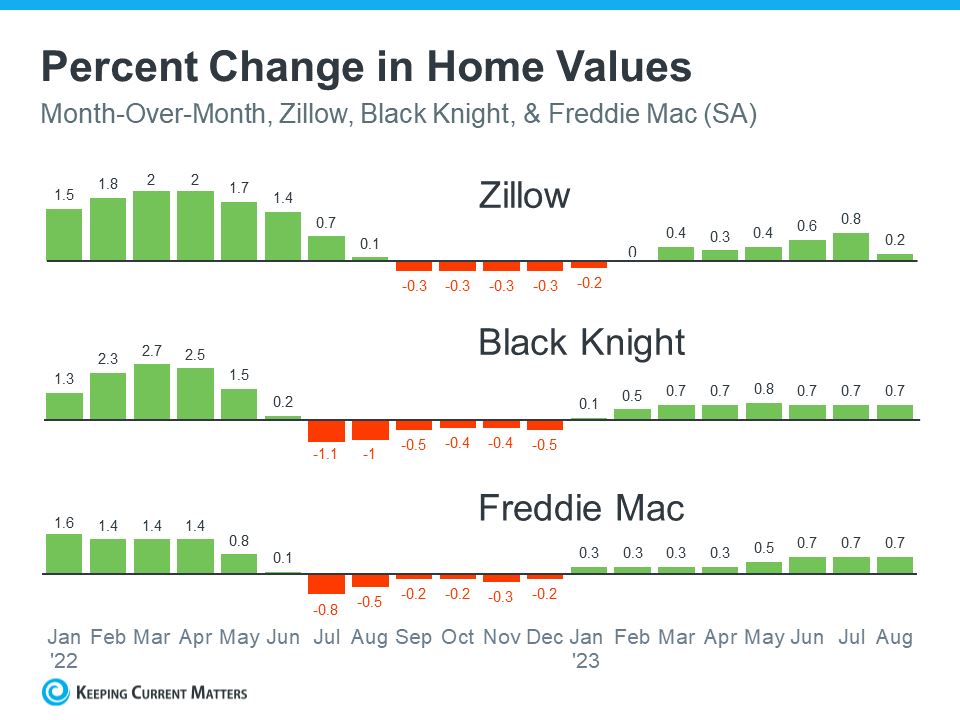

But if you put off moving because you’re worried home prices might drop, make no mistake, they’re not going down. In fact, it’s just the opposite. National data from several sources says they’ve been going up consistently this year (see graph below):

Here’s what this graph shows. In the first half of 2022, home prices rose significantly (the green bars on the left side of the graphs above). Those increases were dramatic and unsustainable.

So, in the second half of the year, prices went through a correction and started dipping a bit (shown in red). But those slight declines were shallow and short-lived. Still, the media really focused on those drops in their headlines – and that created a lot of fear and uncertainty among consumers.

But here’s what hasn’t been covered fully. So far in 2023, prices are going up once more, but this time at a more normal pace (the green bars on the right side of the graphs above). And after price gains that were too high and then the corrections that followed in 2022, the fact that all three reports show more normal or typical price appreciation this year is good news for the housing market.

Orphe Divounguy, Senior Economist at Zillow, explains changing home prices over the past 12 months this way:

“The U.S. housing market has surged over the past year after a temporary hiccup from July 2022-January 2023. . . . That downturn has proven to be short lived as housing has rebounded impressively so far in 2023. . .”

Looking ahead, home price appreciation typically starts to ease up this time of year. As that happens, there’s some risk the media will confuse slowing price growth (deceleration of appreciation) with home prices falling (depreciation). Don’t be fooled. Slower price growth is still growth.

Why Are Home Prices Increasing Now?

One reason why home prices are going back up is because there still aren’t enough homes for sale for all the people who want to buy them.

Even though higher mortgage rates cause buyer demand to moderate, they also cause the supply of available homes to go down. That’s because of the mortgage rate lock-in effect. When rates rise, some homeowners are reluctant to sell and lose their current low mortgage rate just to take on a higher one for their next home.

So, with higher mortgage rates impacting both buyers and sellers, the supply and demand equation of the housing market has been affected. But since there are still more people who want to purchase homes than there are homes available to buy, prices continue to rise. As Freddie Macstates:

“While rising interest rates have reduced affordability—and therefore demand—they have also reduced supply through the mortgage rate lock-in effect. Overall, it appears the reduction in supply has outweighed the decrease in demand, thus house prices have started to increase . . .”

Here’s How This Impacts You

Buyers: If you’ve been waiting to buy a home because you were afraid its value might drop, knowing that home prices have gone back up should make you feel better. Buying a home gives you a chance to own something that usually becomes more valuable over time.

Sellers: If you’ve been holding off on selling your house because you were worried about how changing home prices would impact its value, it could be a smart move to work with a real estate agent and put your house on the market. You don’t have to wait any longer because the most recent data indicates home prices have turned in your favor.

Bottom Line

If you put off moving because you were worried that home prices might go down, data shows they’re increasing across the country. Work with a local real estate agent to understand how home prices are changing in your local area.

Debt — and the way you manage it — can help or harm your ability to buy a home.

If you’re preparing to buy a home in the future, you likely have a laundry list of things you need to do to get ready — and that includes getting your finances in tip-top shape.

Aside from double-checking your credit score and credit report and making sure you have enough money saved up to purchase in your desired market, you should also consider the ways your current debt balance might affect your ability to buy a home.

1) It shows lenders you can handle paying back lenders

Having some debt on your credit report is still really important because lenders need “clues” about how good you are at managing different forms of debt. So having a student loan that you paid off on your credit report can be a green flag to lenders.

Or, maybe you’ve been managing two credit cards really well over the last five years; this is another positive trade line that will show up on your credit report and help you appear less risky as a borrower.

If you don’t have any history of managing debt — even one credit card — lenders may not feel comfortable giving you such a large loan because you lack those clues about your debt management habits.

2) Managing debt well can improve your credit score

Healthy debt management habits can set you up to have an easier time getting approved for your home loan. Not only do you have a history of managing debt, but you also have clues that point to positive management habits — and that can be reflected in your credit score.

Most mortgage lenders look for a credit score of at least 620. Some lenders, like Rocket Mortgage, may still consider applicants who have credit scores of at least 580 for some home loans. But the higher your credit score, the lower your mortgage interest rate will be. That’s why working to improve your credit score before you apply can work to your advantage.

Payment history makes up 35% of your credit score. So just by consistently making your credit card, auto loan, and other payments every month, you’re contributing to improving your credit score. Likewise, if you were to miss a payment, this could have a big impact on your credit score.

The amount of money you owe is the second most important factor in determining your credit score (it makes up 30% of your score). This is usually a measure of your credit utilization, which is the amount of money you owe in relation to your total credit limit. Experts typically recommend keeping your credit utilization below 30%.

So if you have $5,000 as a total credit limit and owe $2,500, your credit utilization is 50% and it would be a good idea to continue making payments so you can lower your utilization.

Because of that credit utilization rate, carrying too much debt could drag down your credit score. Coming close to maxing out your available credit makes lenders think that you’re spending beyond your means and would therefore be a risky borrower.

3) Having too much debt can make you ineligible for some home loans

One criteria mortgage lenders assess when reviewing your home loan application is known as the debt-to-income ratio. Your debt-to-income ratio is a comparison of how much you owe to how much money you earn. Your gross income (pre-tax income) is used to measure this number.

A lower debt-to-income ratio suggests that you have a healthy balance between debt and income. However, a higher debt-to-income ratio suggests that too much of your income is going toward paying down debt, and this will make a mortgage lender see you as a risky borrower.

According to a breakdown from The Mortgage Reports, a debt-to-income ratio of no more than 43% is considered good; a ratio closer to 45% might be acceptable depending on the loan you apply for, but a ratio that’s 50% or higher can raise some eyebrows.

A higher debt-to-income ratio could make you unable to be approved for some home loan programs with attractive features, like lower down payment minimums. For instance, the HomeReady loan program from Ally Bank requires applicants to have a debt-to-income ratio of no more than 50%, among other criteria.

If you want to calculate your debt-to-income ratio, here’s what you do: Add up all your monthly debt payments, which include credit card payments, student loan payments, and payments to any other lines of credit you may have. Then Divide this number by your gross income amount. The result is your debt-to-income ratio.

How to consolidate and best payoff debt

If you have an unhealthy amount of debt and are preparing to get a mortgage, consider these strategies to consolidate and pay down your debt.

The debt snowball method is one debt management method where you focus on eliminating the smallest debt balance first while paying just the minimum on all your other debts. On the other hand, the debt avalanche method involves eliminating your highest-interest debt first. Both methods can be instrumental in helping you crush your debt balance in a more organized way.

Debt consolidation is another popular method for paying down debt if you carry balances on multiple credit cards or have multiple loans. Essentially, you’ll apply for a personal loan that’s enough to cover the total amount of debt on all your credit cards. Then, once you’re approved, the lender sends the funding amount to your creditors, which pays off your credit cards. From there, you’ll just have to pay back the personal loan you borrowed.

This method can potentially help you save on interest since personal loan lenders typically offer much lower interest rates compared to credit card issuers. The Happy Money personal loan is one of the best debt consolidation loans out there since this lender will send your funds directly to creditors.

Balance transfer credit cards with a 0% intro APR period are another useful option for getting rid of debt since these credit cards allow you to make interest-free monthly payments for a limited time. Interest charges can eat into your monthly payments and make it feel like your balance is barely going down. With this method, you basically transfer the balance of your current credit card onto a new credit card and you try to pay off the balance before the interest-free period is over.

The Citi® Diamond Preferred® Card offers an intro APR period of 0% for 21 months on balance transfers (after, the 18.24% – 28.99% variable). So you’ll basically have almost two years to make interest-free credit card payments. Just keep in mind that you’ll have to pay a 5% transfer fee on each balance that you transfer ($5 minimum). Balance transfers must be completed within 4 months of account opening.

The Wells Fargo Reflect® Card also offers an intro APR period of 0% for 21 months from account opening on purchases and qualifying balance transfers (after, 18.24%, 24.74%, or 29.99% variable). Balance transfers made within 120 days from account opening qualify for the intro rate, BT fee of 5%, min $5.

Bottom line

Having experience managing debt in a healthy manner can help you get approved for a mortgage, but the key here is to make sure you’re practicing positive habits with your debt. Continue making on-time monthly payments toward your debts, don’t let your credit utilization rate get too high, and be wary of the amount of debt you have in relation to how much you earn.

Learn strategies for saving a down payment, applying for a mortgage, shopping for a house, and more.

It’s exciting — and a little scary — to think about buying your first home. Even when you know you’re ready to buy a house, you might not be sure where to begin. These tips for first-time home buyers will help you navigate the process from start to finish.

Preparing to buy tips

1. Start saving early

When calculating how much money you need to buy a house, consider one-time expenses as well as new, recurring bills. Here are the main upfront costs to consider when saving for a home:

Down payment: Your down payment requirement will depend on the type of mortgage you choose and the lender. Some conventional loans aimed at first-time home buyers with excellent credit require as little as 3% down. But even a small down payment can be challenging to save. For example, a 3% down payment on a $300,000 home is $9,000. Use a down payment calculator to decide on a goal, and then set up automatic transfers from checking to savings to get started.

Closing costs: These are the fees and expenses you pay to finalize your mortgage, and they typically range from 2% to 6% of the loan amount. Your closing costs on a $300,000 loan could be between $6,000 and $18,000. That’s additional money you’d have to pay, on top of your down payment. In a buyer’s market, you can often ask the seller to pay a portion of your closing costs, and you can save on some expenses, such as home inspections, by shopping around.

Move-in expenses: Remember to budget for moving costs, which typically run up to $2,500 for most local moves. (Long-distance moves can be much pricier.) You’ll need some cash after the home purchase. Set some money aside for immediate home repairs, upgrades and furnishings.

2. Decide how much home you can afford

Figure out how much you can safely spend on a house before starting to shop. NerdWallet’s home affordability calculator can help with setting a price range based on your income, debt, down payment, credit score and where you plan to live.

3. Check and polish your credit

Your credit score will determine whether you qualify for a mortgage and affect the interest rate lenders will offer. Having a higher score will generally get you a lower interest rate, so take these steps to polish your credit score to buy a house:

Get free copies of your credit reports from each of the three credit bureaus — Experian, Equifax, and TransUnion — and dispute any errors that could hurt your score.

Pay all your bills on time, and keep credit card balances as low as possible.

Keep current credit cards open. Closing a card will increase the portion of available credit you use, which can lower your score.

Avoid opening new credit accounts while you’re applying for mortgages. Opening new accounts could put a hard inquiry on your credit report and lower the overall average age of your credit accounts, which could hurt your score.

Standard inspections don’t test for things like radon, mold or pests. Understand what’s included in the inspection and ask your agent what other inspections you might need.

Make sure the inspectors can get to every part of the house, such as the roof and any crawl spaces.

An existing home generally costs less than buying a new construction home. But if local inventory is low and you have the means, a brand-new home offers enticing options to customize.

A condominium or townhome may be more affordable than a single-family home, but shared walls with neighbors will mean less privacy. Don’t forget to budget for homeowners association fees when shopping for condos and townhomes, or houses in planned or gated communities.

A manufactured home, including the type commonly called a mobile home, can be an affordable option if you have a tight budget. You’ll need to title it as real property and affix it to a permanent foundation if you want to finance it with a traditional mortgage. Many manufactured homes are financed through chattel loans, which have higher interest rates than mortgages.

Fixer-uppers, or single-family homes in need of updates or repairs, usually sell for less per square foot than move-in-ready homes. However, you may need to budget extra for repairs and remodeling. Renovation mortgages finance both the home price and the cost of improvements in one loan.

The buyer doesn’t have to attend the inspection, but it could be useful to be there. By following the inspectors around you can get a better understanding of the home and ask questions on the spot. If you can’t attend the inspections, review the reports carefully and ask about anything that’s unclear.

4. Explore mortgage options

A variety of mortgages are available with varying down payment and eligibility requirements. Here are the main categories:

Conventional mortgages are the most common type of home loan and are not guaranteed by the government. Some conventional loans targeted at first-time buyers require as little as 3% down.

FHA loans are insured by the Federal Housing Administration and allow down payments as low as 3.5%.

USDA loans are guaranteed by the U.S. Department of Agriculture. They are for suburban and rural home buyers and usually require no down payment.

VA loans are guaranteed by the Department of Veterans Affairs. They are for current military service members and veterans and usually require no down payment.

You also have options when it comes to the mortgage term. Most home buyers opt for a 30-year fixed-rate mortgage, which is paid off in 30 years and has an interest rate that stays the same. A 15-year loan typically has a lower interest rate than a 30-year mortgage, but the monthly payments are larger.

If you plan to stay in the home for only a few years, you might consider an adjustable-rate mortgage or ARM. ARMs often start with a lower fixed-interest introductory rate, enabling you to buy a more expensive home for the same monthly payment, but they can also increase (or decrease) over time.

5. Research first-time home buyer assistance programs

Many states and some cities and counties offer first-time home buyer programs, which often combine low-interest-rate loans with down payment assistance and closing cost assistance. If you meet low- to moderate-income benchmarks, you could qualify for a grant or forgivable loan that doesn’t need to be paid back.

Tax credits, known as mortgage credit certificates, are also available through some first-time home buyer programs.

6. Compare mortgage rates and fees

Plan to shop around for mortgage lenders and compare three to five different quotes. Doing so could save you thousands of dollars in interest over the lifetime of the loan.

The Consumer Financial Protection Bureau recommends requesting loan estimates for the same type of mortgage from multiple lenders to compare the costs, including interest rates and possible origination fees.

Lenders may offer the opportunity to buy discount points, which are fees the borrower pays upfront to lower the interest rate. Buying points can make sense if you have the money and plan to stay in the home for a long time. Use a discount points calculator to decide.

In a buyer’s market, some motivated sellers may offer to pay some or all of the buyer’s points to close the deal.

7. Gather your loan paperwork

Before you’re approved for a mortgage, your lender will ask you for financial records to verify your income, assets, and debt, including:

Proof of income and employment, such as tax returns, W-2s and 1099s.

Statements for bank, retirement, and brokerage accounts.

Records of debt payments, such as student loans, auto loans, or any real estate debt.

Documentation of other events that impact your finances, such as divorce, bankruptcy, or foreclosure.

Pull these documents ahead of time to stay organized throughout the process — you’ll need them for a mortgage preapproval as well as when you apply for the loan.

8. Get a preapproval letter

A mortgage preapproval is a lender’s offer to loan you a certain amount under specific terms. Having a preapproval letter shows home sellers and real estate agents that you’re a serious buyer and can give you an edge over home shoppers who haven’t taken this step yet.

Apply for preapproval when you’re ready to start home shopping. A lender will pull your credit and review the documents you organized in the previous step. Applying for preapproval from more than one lender to shop rates shouldn’t hurt your credit score as long as you apply for them within a limited time frame, such as 30 days.

Home shopping tips

9. Choose a real estate agent carefully

A good real estate agent will scour the market for homes that meet your needs and guide you through the negotiation and closing processes. Get agent referrals from other recent home buyers. Interview at least a few agents and request references. When speaking with potential agents, ask about their experience helping first-time home buyers in your market and how they plan to help you find a home. You might also ask how they find homes that aren’t yet on the market, which can be a handy skill when buyer competition is fierce.

10. Narrow down your ideal type of house and neighborhood

Weigh the pros and cons of different types of homes, given your lifestyle and budget.

Think about your long-term needs and whether a starter home or forever home will meet them best. If you plan to start or expand your family, it may make sense to buy a home with extra room to grow.

Research potential neighborhoods thoroughly, including property values, property taxes, and safety considerations. Choose one with amenities that are important to you, including schools and entertainment options. If you work away from home, test out the commute during rush hour.

11. Stick to your budget

To avoid financial stress down the road, set a price range based on your budget — and then stick to it.

A lender may offer to loan you more than what is comfortably affordable, or you may feel pressure to spend outside your comfort zone to beat another buyer’s offer in a bidding war.

In a competitive market, consider looking at properties below your price limit to give some wiggle room for bidding. In a buyer’s market, you may be able to view homes a bit above your limit. Your real estate agent can suggest a range for your offering price.

12. Make the most of walk-throughs and open houses

Online 3D home tours have become more popular as technology improves. They don’t supply all the information in-person visits do — like how the carpets smell — but they can help you narrow the list of properties to visit.

It’s possible to buy a house sight unseen, but it’s always best to visit in person. Open your senses when walking through a home. Listen for noise, pay attention to any odors, and look at the overall condition of the home inside and out. Ask about the type and age of the electrical and plumbing systems and the roof.

Home purchasing tips

13. Don’t skip the home inspections

A home inspection is a thorough assessment of the structure and mechanical systems. Professional inspectors look for potential problems, so you can make an informed decision about buying the property. Here are some things to keep in mind

14. Negotiate with the seller

You may be able to save money by asking the seller to pay for repairs in advance or lower the price to cover the cost of repairs you’ll have to make later. You may also ask the seller to pay some of the closing costs. But keep in mind that lenders may limit the portion of closing costs the seller can pay.

Your negotiating power will depend on the local market. It’s tougher to drive a hard bargain when there are more buyers than homes for sale. Work with your real estate agent to understand the local market and strategize accordingly.

15. Buy adequate home insurance

Your lender will require you to buy homeowners insurance before closing the deal. Home insurance covers the cost to repair or replace your home and belongings if they’re damaged by an incident covered in the policy. It also provides liability insurance if you’re held responsible for an injury or accident. Buy enough home insurance to cover the cost of rebuilding the home if it’s destroyed.

It may be worth buying an umbrella policy if you need to cover your home, cars, and other major assets.

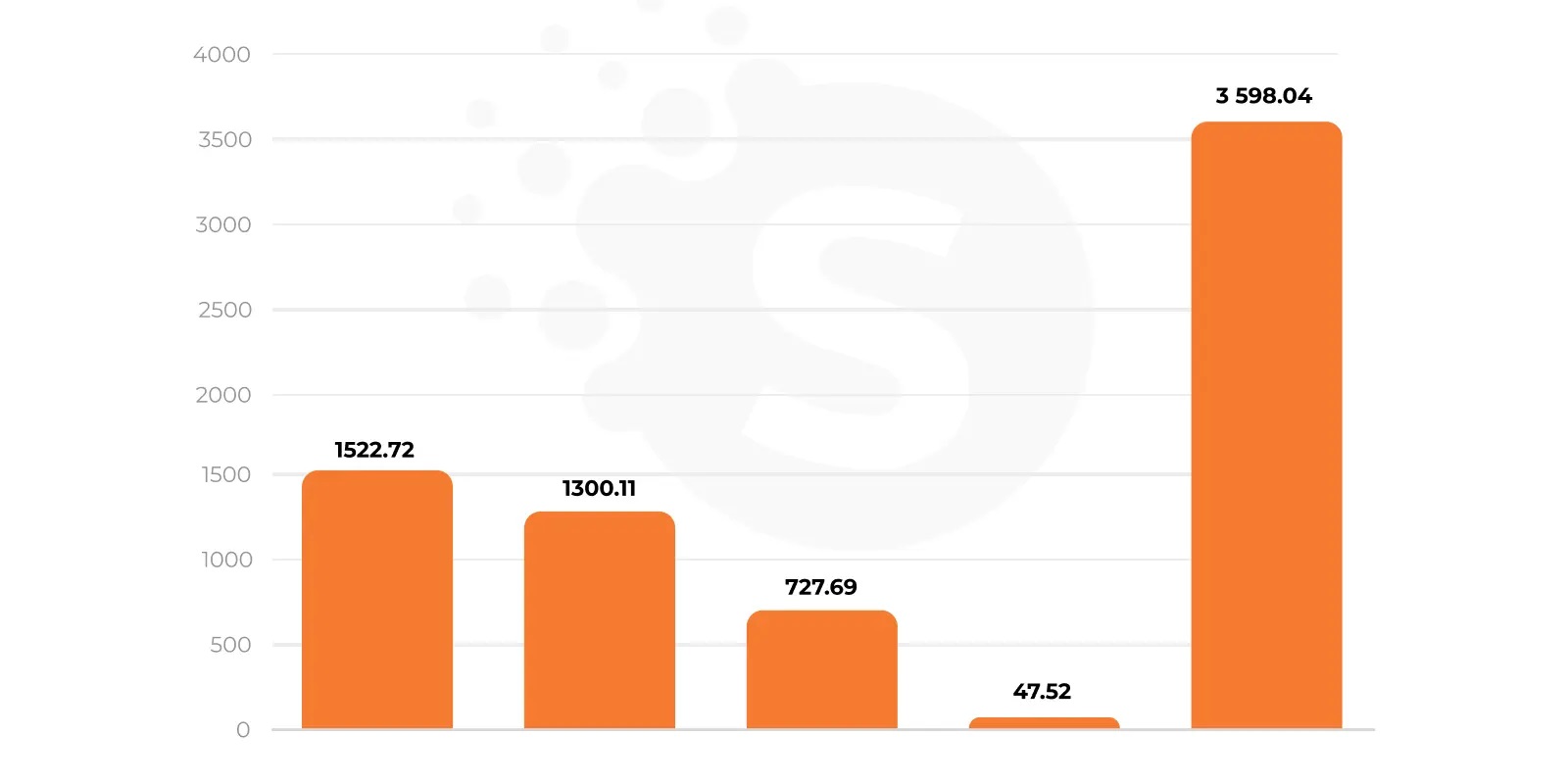

Real estate technology has been rapidly evolving in recent years, and the introduction of cutting-edge technologies in real estate promises to change the way business is conducted in this age-old industry. The real estate market is a major component of the world’s economy, with a global value of over $7 196 billion.

Real Estate Tech Trends 2022

In some respects, the adoption of technology in real estate has lagged behind its use in other business sectors. It was partially due to a reluctance to change methods that had worked well in the past. Another factor that slowed down the widespread use of real estate technology was major players’ attempts to develop proprietary real estate technology tools.

But now, these issues are fading, and the market has seen an increase in real estate tech in recent years.

Moreover, the industry players are starting to understand the benefits of investing and using modern technologies. According to the Technology and The Future of Real Estate Investment Management report created by the University of Oxford, in 2020, 53% of digital real estate companies are now directly investing in technology. 42% of Statista respondents confessed they see potential in Smart Building technologies, while 56% of respondents have already noticed the impact from the tech sphere.

Real Estate Innovations in 2022

It is poised to see even more growth in how new technologies are genuine real estate disruptors and will affect everyone involved in the industry.

What Is Proptech: Industry Overview

Proptech is a rather amorphous term that is formed from the words property and technology. It encompasses the various solutions that are involved in the growth of commercial real estate software.

Proptech is also known as CREtech for commercial real estate technology or REtech for real estate technology. It usually refers to the software employed in real estate tools and applications.

Six months through 2021, VC deal activity in residential real estate tech has already reached an annual record of $6.2 billion, according to PitchBook data. And with $2.6 billion in funding, the commercial segment is on track to make 2021 the second-most valuable year for venture activity.

The industry shows no signs of slowing down with new generations of consumers and realtors opting for smart solutions that facilitate faster rentals and more convenient living arrangements.

Real Estate Technology Trends For 2023 That Disrupt the Industry

The successful adoption of a specific technology in the real estate industry will be determined by its ability to provide value for its users.

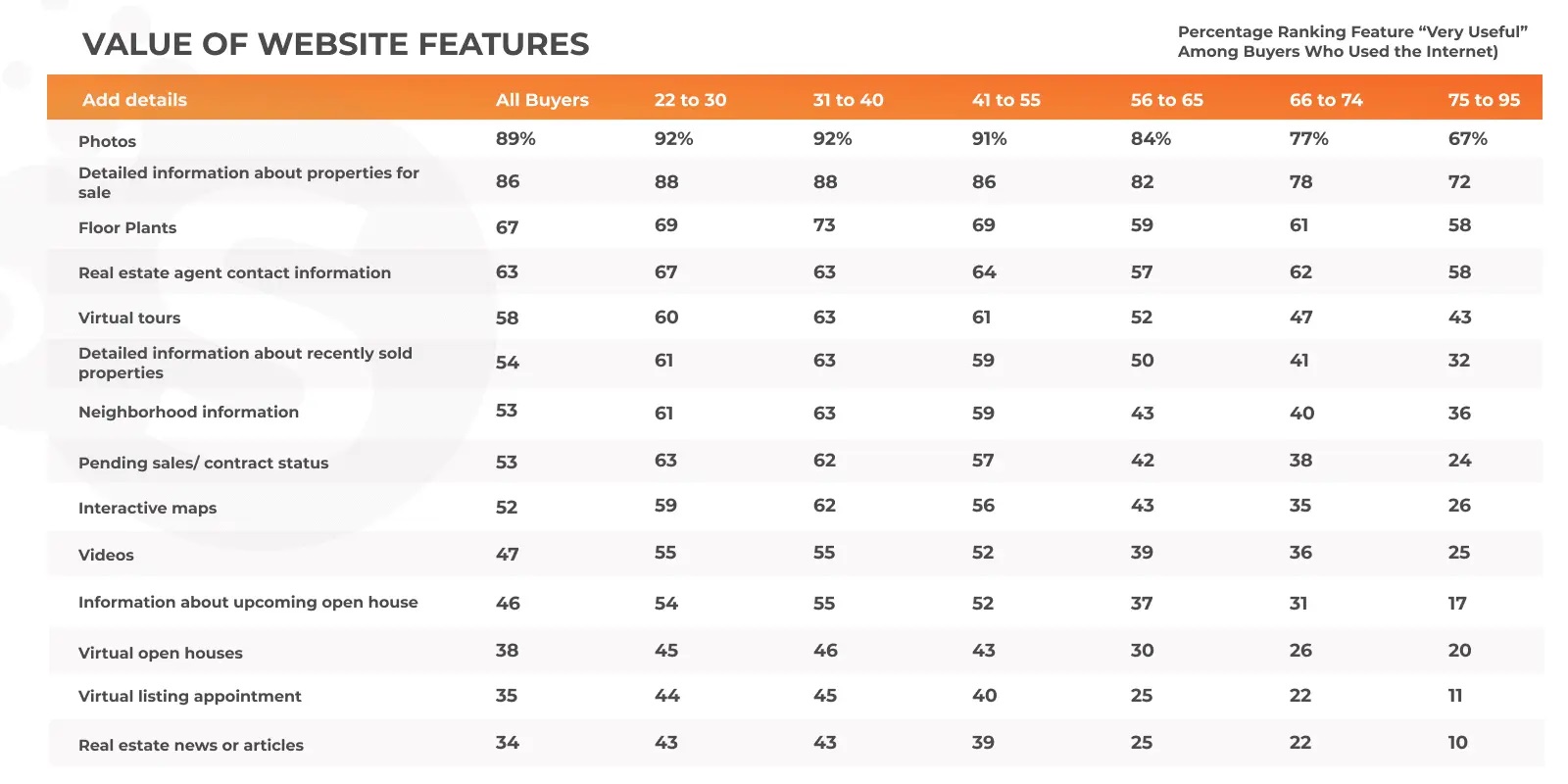

According to the 2021 NAR Home Buyer and Seller Generational Trends report, certain features are important to users. Photos, detailed information, floor plans, real estate agent contacts, and virtual tours are among them.

Real Estate Tech Trends 2023

Technologies help to cover the users’ needs and bring them valuable information they use for decision-making.

Automated Rental and Purchasing Property Platforms

This real estate innovation is truly changing the industry. Nowadays, how clients find the new property they bought is changing to the Internet more than meeting with real estate agents.

The benefits of using automated property technologies are overwhelming. Consumers and real estate professionals will be at a distinct disadvantage if they choose not to use these valuable real estate technology tools to find or sell a home.

3D Virtual House and Apartment Tours

Closely associated with search applications are solutions that enable prospective buyers to take a virtual tour of properties while selecting. It is among the main tech trends in real estate for 2023 as it eliminates the time and expense of visiting multiple properties, many of which can be removed from the buyer’s list of potential purchases through virtual viewing.

Of course, most buyers will want to tour the property before making a final decision physically. Still, the time and money savings for the customer and real estate agent in determining the best fit can quickly add up. Moreover, today VR technologies allow having almost realistic virtual tours to houses where you can easily examine the property state, interior details, and furniture. And the real estate photo editing services allow to make photos as true to life as possible.

Real estate software customers expect to get the best service and experience from using the technologies. Contact channels must be available 24/7, the response time must be as fast as possible, and the error rate should be close to zero.

An automated service desk with the conversation AI can easily fulfill the requirements. This technological approach goes beyond common chatbots making it one of the main real estate innovations in 2022. According to Deloitte, ‘these assistants would be built for purpose, have a rich set of capabilities, and be integrated into the end-to-end process landscape of the enterprise.’

Big data

Databases and data warehouses are used to store the immense quantities of information that is gathered concerning consumer preferences.

According to McKinsey’s research, real estate applications based on machine-learning models can predict changes in rent rate with 90% accuracy, while the changes in other property metrics can predict with 60%. That can pretty well help clients understand what property is a better choice for their investment, as in the case of commercial property and non-commercial.

Blockchain

Tech-savvy readers may not immediately make the connection between blockchain technology and real estate. While many individuals are familiar with how the blockchain is used in cryptocurrency, it has wide applications in other areas of commerce, including the real estate industry.

Blockchain technology can be used to verify encrypted transactions and ensure that no tampering impacts financial records. It will prove useful in fractional property investment and allow landlords to sell portions of their stake in a given holding.

The property technology will also enable important documents such as property titles to be stored securely. As with other market sectors, the surface has only been scratched as far as the potential in employing the blockchain for other cases in the real estate industry makes it one of the top real estate tech trends in 2023.

Fractional Property Investment

Fractional ownership refers to percentage ownership in an asset. It is a common investment strategy when purchasing expensive items such as aircraft or vacation homes. Using the blockchain mentioned above technology, fractional property investment is flourishing for a variety of reasons.

The high price of homes put them out of reach to many would-be buyers. Fractional property investment allows these individuals or groups to build a deposit on a future full purchase.

Communal investors can all share rental income from a shared property, opening up an additional income stream. Employing a fractional ownership approach will enable more diversified investment and allow people to unlock the value in their homes.

Mobile Apps

One of the most efficient technologies used in the industry is mobile, e.g., developing different real estate apps. The most popular ones are rental and purchasing mobile platforms.

These apps offer several advantages to potential renters over the traditional means of locating an apartment or house. Databases are frequently updated, providing more timely information on new properties put on the market and those that are no longer available.

Consumers interested in purchasing, selling, or renting a property can also use apps tailored to their needs. They can help you locate the house you want and put you in touch with a real estate agent to help facilitate the deal.

Internet of Things (IoT)

Smart homes, apartments, and devices are changing the way we live in many ways. Smart devices, in general, are powered by the Internet of Things (IoT) and are becoming one of the main property management technology trends.

The IoT refers to the practice of embedding sensors and computing technology into various items with which we interact every day. The ultimate goal of this technology is to provide individuals with a more convenient and pleasurable life.

Let’s investigate in what way IoT technologies are changing our homes and transform them into smart homes. There are three main characteristics of a smart apartment:

Smart amenities include devices such as smart lights and locks and integrated services like home cleaning and package delivery.

Connectivity is designed into a smart apartment when it is built to enable devices, building systems, residents, and management to communicate. Items such as WiFi, smart sensors, and intelligent access controls are benefits afforded by enhanced connectivity.

Community management by providing services that save residents time, money, and minor difficulties is the final component of a smart apartment. Built-in event calendars, resident assistance, and on-demand services are some of the features that help property managers and renters build a more vibrant community.

By the way, this is one of the most demanded trends in proptech for apartment websites and real estate platforms. While new construction is prime territory for implementing smart apartments, older structures can be retrofitted to provide the same level of connectivity.

Analytics and data management

Among other tech trends impacting real estate, it is worth mentioning data management. Data will influence decisions, and since there is still no centralized national system for agents, new startups will have unlimited opportunities to develop and change the existing process. Accordingly, now is the perfect time to create an innovative solution in this industry. You can build an application that will analyze a huge amount of data to provide valuable information necessary for decision-making by real estate market participants. For example, your solution might show the level of reliability of a developer and their buildings.

Digital twins

As more information is made available online, prospective buyers will have more opportunities to study and explore properties. Imagine seeing a 3D digital model of each building when looking for housing. Such applications will make predictions of the critical parameters of environmental conditions that a particular house can withstand (earthquakes, tornadoes, landslides, etc.). Maintain companies will know the current conditions of buildings (existing and potential damage, date, and place of repair) and fire escape plan.

Moreover, digital twins can be useful during constructing houses, which helps the developer understand how safe their project will be. Such applications can prevent the collapse of buildings and use developers’ resources rationally.

Direct digital engagement

More touchless services are offered to end-users, resulting in a safer and healthier process. Traditional procedures, such as in-person home tours, would be automated due to direct digital interaction and disruptive technology in real estate. Buyers and real estate agents will no longer need to travel to every apartment or house to make a decision. Therefore, photos, digital brochures and virtual tours should be of high quality. Thus, people can see each element in detail.

But it’s much more important when, in applications, buyers can look at houses that are still under construction. At the same time, the developer posts photos every month about the state of the future building, increasing its reliability in the buyers’ eyes, thus making direct engagement one of the most popular digital trends in real estate.

Digital Transaction Management

That’s one of the important property technology trends, and we recommend paying attention to it. Buyers and agents value their time. Thus, you can create a solution to remove paperwork and enable signing documents electronically. Consequently, the parties to the transaction can be in different parts of the world and still access the contracts from any device.

Hyper-personalized messages

Among emerging technologies in real estate, this is another very interesting one. Datasets and predictive analytics allow agents to understand their customers better and group them with those who share similar lifestyle characteristics. As a result, agents can now build highly targeted messages and content that target particular audiences. They send emails to describe the housing, the benefits, and the documents needed to conclude a deal. What’s more, agents use Facebook and Instagram to conduct tours of apartments or houses. They can also create their own YouTube channel, where they talk about the latest news on the real estate market, share life hacks in this industry, and much more.

Lead generation and engagement automation

Conversation chatbots powered by artificial intelligence will initiate conversations and respond instantly to inquiries. It will assist agents in capturing, engaging, and qualifying online leads. These bots will also manage the initial stages of working with a potential customer using natural language processing. This technology helps agents be with their customers 24/7 and get new leads they connect with during business hours.

These trends in real estate have been very helpful throughout 2023 and in our view will continue to be relevant in 2023.

Essential Technology for Real Estate Agents

Some technological innovations are equally important to consumers and real estate professionals. Today, real estate agents begin to use specific technology for realtors designed to help them provide services to their clients. Here are some popular real estate agent technology tools that are in use today:

Multiple Listing Services (MLS)

In-app communication

Social media

Advertising automation

Ad campaigns for new listings can now be generated automatically by software systems. They can also display ads to the appropriate audiences and include real-time statistics such as views, clicks, and demographics. Real estate agents can understand which housing is best for sale or rent. And accordingly, they concentrate their efforts on the objects that bring them the most profit.

Robotic process automation

Real estate transactions can be challenging to handle, especially when it comes to communication. New technologies are being implemented to fix these issues that allow two groups of users to communicate online. Real-time chat, file sharing, and transaction tracking will also be possible. You can also develop an application where potential buyers can solve some of their small questions using a chatbot, significantly saving real estate agents’ time.

Or, you can create an AI-powered Virtual Assistant solution where a customer interacts with a robot that speaks like a human. This assistant can connect potential clients already with a real agent for deeper discussions of real estate issues. Sensely has done something similar in the healthcare industry (a virtual nurse app).

High-Tech Devices in the Real Estate Industry

The innovative use of new technology in real estate has been incorporating drones into showcasing and selling homes. Here are some of the advantages that drones offer real estate agents and those buying and selling homes: