The next five years will likely usher in slower increases in both home prices and rents.

Key Takeaways

-

- Sales of existing homes will grow moderately as buyers become accustomed to higher prices and mortgage rates, but transactions could surge if rates decline.

- New policies on real estate commissions and the sharing of home listings on public MLS systems will likely vary between regions before revamped national rules are enforced.

- Newly built homes will continue to fill in the supply gaps created by the lack of existing home inventory, especially by homebuilders who can buy down mortgage rates.

- Mortgage rates will likely range from about 6% to 7% unless there is a recession, but short-term lending rates will continue falling through 2026.

Over the next five years, with fallout from the COVID-19 pandemic gradually giving way to potential impacts from a second Trump administration, look for changes to immigration, expanding tariffs, the rising costs of damages related to climate change, the expansion of AI into more parts of our daily lives and the steady dissolution of the rules-based international order focused on global trade flows.

Still, for the housing market, none of these factors will weigh as heavily as mortgage rates: If they remain relatively high, transactions will be based more on households making moves due to changes in jobs, finances or household composition. However, if mortgage rates manage to fall faster, then pent-up demand from the last few years could be unleashed with volumes returning more to historic norms. How this plays out will determine just how different the list of the hottest housing markets in 2029 may look versus 2024.

Our data is sourced from several authoritative sources, including the U.S. News Housing Market Index, an interactive platform providing a data-driven overview of the housing market nationwide.

Housing Index Score over Time

Existing Home Sales Will Rise but Still Be Constrained

In comparison with historical norms prior to the pandemic years, home sales are expected to remain low as long as mortgage rates remain well over the 6% level. According to recent projections, the Federal Reserve doesn’t see inflation subsiding to 2.0% on a consistent basis until early 2026. This will mean higher but gradually declining short-term interest rates throughout 2025.

Interest Rates | 6.18% (-1.02% YOY)

Two other wild cards include the potential impact of tariffs and the deportation of millions of undocumented immigrants, both of which could be destabilizing to the economy – especially in agriculture and construction – and lead to a rebound in inflation. Since mortgages are influenced much more by the 10-year Treasury bond than the Fed’s short-term rates, if investors demand higher bond rates in exchange for additional risk, that reduces the Fed’s influence on long-term mortgage rates and rates could stay elevated.

Still, given that consumers have become more used to higher borrowing rates for homes, those with sufficient incomes and down payments may see 2025 as a perfect year to jump back into the housing market, especially as the lock-in effects of sub-6% interest rates continue to wane.

As of the second quarter of 2024, although nearly 86% of homeowners with mortgages had interest rates below 6%, that share is down from nearly 93% two years ago and continues to decline as sellers are forced to list their homes for a variety of reasons such as job changes, the need for more space as well as the three Ds: death, divorce and debt.

Rob Cook, Chicago-based vice president and chief marketing officer for Discover Home Loans, advises existing homeowners looking to sell to first compare their existing and future mortgage payments, and perhaps consider renovation as an option.

“A home equity loan could be an appealing option for financing home improvement projects, as it allows current homeowners to use the available equity they’ve built in their homes without modifying their existing mortgage,” he said in an emailed response. For those who need to move, he suggests other options aside from the traditional fixed-rate mortgage. “If rates remained elevated, there could be increased demand for ARMs (adjustable-rate mortgage) or other variable rate products. Homeowners should be mindful of how these types of mortgages could result in higher rates in the future.”

With the November election in the rearview mirror, potential homebuyers are already preparing well in advance of the traditional spring selling season: Redfin’s Homebuyer Demand Index, which tracks tours and other services requested from its agents adjusted for seasonality, was up 7% year-over-year during the first week of December to approach its highest level since September 2023. In addition, the Fannie Mae Home Purchase Sentiment Index rose again in November to its highest level since February 2022, as well as rebounding sharply from the all-time survey low set just over two years ago.

Median Sales | $429k (+4.1% YOY)

Median Rent Price | $2,050 (+1.8% YOY)

Housing Supply | 3.1 mo (+0.55 YOY)

Rental Vacancy | 6.3% (+0.4% YOY)

Homebuilders Will Reap Supply Shortage Benefits

If the inventory of existing housing supply remains relatively low, buyers will continue to instead look for newly built homes. With newly built homes making up about 30% of overall housing inventory in recent months (or approximately double its historic share) more buyers are considering the advantages of new construction. Housing starts jumped from under 1.3 million in 2019 to over 1.5 million in 2022 before settling back to an annualized rate of about 1.3 million in October.

Buyers of new homes will certainly have ample options from which to choose, with months of supply for new single-family homes rising to 9.5 months in October – more than double the level of existing single-family supply of 4.2 months. About one-quarter of these unsold new homes have completed construction, which could be great news for buyers in search of a deal. That’s because larger builders interested in selling off their inventory also have the financial resources to offer generous incentives, such as mortgage rate buydowns, paying for closing costs and providing allowances at their design centers.

Doug Bauer, CEO of the leading homebuilder Tri Pointe Homes in Irvine, California, is certainly bullish on new home construction. “We’re planning on a strong spring selling season,” he says. “(Mortgage) rates may hover around 7% and we have the levers and tools to meet pretty unmet demand.”

As for the potential impact of deportation of undocumented construction workers, Bauer says that it is unlikely to impact the majority of native-born or documented skilled tradespersons working with the larger public homebuilders. However, the ongoing issue of future shortages in the construction trades continues to be addressed by foundations such as the Home Builders Institute.

Looking further along into the forecast period, Bauer also sees the reduction of energy-efficient building codes recently mandated by HUD and USDA when financing new residential construction as an important step to improving affordability. According to a study cited by the NAHB, building to the 2021 International Energy Conservation Code can add over $30,000 to the price of a new home. Should these mandates be extended to mortgage giants Fannie Mae and Freddie Mac – which together finance 72% of new home purchases – new home affordability would be impacted across the country.

Single-Family Building Permits

Multi Family Building Permits

Real Estate Commission Procedures Will Change

Now that National Association of Realtors (NAR) has rolled out new rules on real estate commissions to most multiple listing services nationwide, the ways in which sellers and buyers compensate agents will change and potentially be reduced, especially for luxury housing, in which the actual dollar amounts for these commissions allow room for more negotiations.

Still, there are still some unsettled questions, including some recent appeals of the national agreement and how the Justice Department under a second Trump term plans to enforce it or push for additional industry reforms. For now, however, some industry leaders have opted to simply make it easier to adhere to the agreement as written.

When Leo Pareja was sworn in as CEO of eXp Realty in early April 2024, just three weeks had passed since NAR had reached an agreement with plaintiffs on broker commissions. By late July, with new practices scheduled to go into effect on Aug. 17, Pareja and his team a new listing form a new listing form which clearly states that there is no commission sharing with a buyer’s agent. Given the chaos continuing to embroil the industry at the time, eXp, as the largest residential real estate brokerage in the United States by agent count and transaction sides with operations in over 20 other countries, also encouraged other brokerages to use or even improve upon the form.

“I equated this more to a ‘Y2K’ moment and we went all in. We had to be very clear, consumer friendly without legalese, and educate agents on possible paths,” Pareja says. “It was bumpier in other parts of the country, with a lot of confusion coming out the other way, and had we not jumped on it, it could have played out quite differently.” The Consumer Federation of America seemed to agree: Although critical of the new form introduced by the California Association of Realtors, it not only singled out eXp’s version but also continues to offer it on their own website. The listing site Zillow has also introduced its own Tour Agreement.

Here’s what potential homebuyers should know: Where in the past they could count on a buyer’s agent to spend the day showing listings without any official relationship, they will now be asked to sign a form to create one for a specific period of time. If, however, the agent only shows properties and no purchase offers are made, then no brokerage fees are due.

The Clear Cooperation Policy for MLS listings Is Under Duress

If there’s one more settlement to be made, Pareja thinks it’s regarding the Clear Cooperation Policy, which was introduced by the NAR in 2020 to require listing brokers to submit new listings quickly to their local MLS to provide the widest array of choices to potential buyers.

However, there is a special office exclusive exception for listing brokers who can register the property but not list it as either “active” or “coming soon” as long it is not marketed publicly – sometimes referred to as a “private” or “pocket” listing shared only with a select group of agents (often with the same brokerage to maximize commissions). Since enforcement of the rules are done at the local level, some brokers opt to never register the listing in the MLS at all. Not surprisingly, several large brokerages and local listing systems would like to see the CCP completely reformed.

Although Pareja doesn’t have a problem with the office exclusive exception, he does argue that when brokers refuse to share listings on the MLS while continuing to pull publicly available listings from the same platform for their own websites and clients, that could be problematic in several ways.

Firstly, it could undermine trust in the world’s most efficient market for real estate listings in the United States and Canada, as it would no longer be comprehensive. In most other countries, buyers need to comb through multiple websites of competing brokers to accomplish what the MLS does with a single click. Secondly, it could encourage the hoarding of listings as the primary business proposition of a brokerage at the expense of providing the best value and service. Thirdly, it could do away with the traditional rules of engagement included as part of buying and selling homes listed on the MLS, potentially leading to unnecessarily messy – or even fraudulent – transactions.

Even though a large brokerage such as eXp could flourish with its own private listings, Pareja thinks disbanding the CCP would ultimately be bad for buyers, sellers and agents.

Total Cost of Ownership Will Become More Important

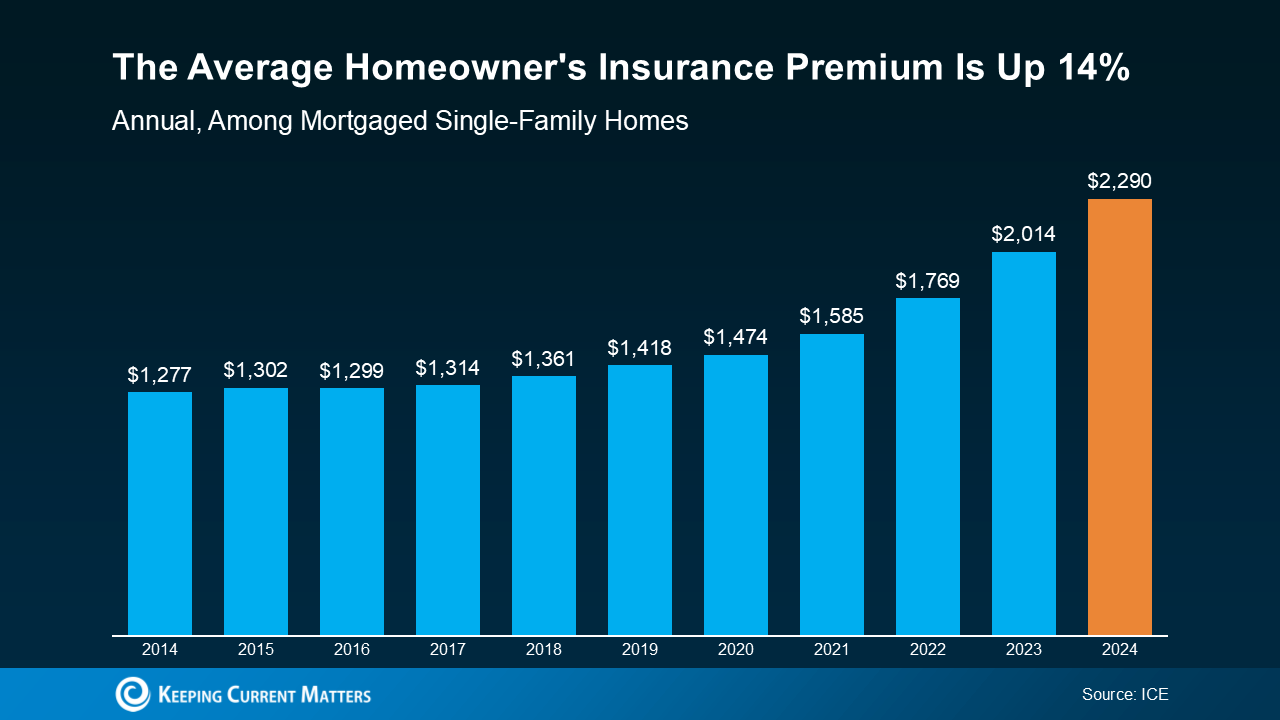

With rising costs for property taxes, home insurance, maintenance and adapting to a changing climate, the total costs for homeownership are far more than just mortgage principal and interest payments alone.

According to a study in mid-2024 by Bankrate, these annual variable costs for a typical single-family home rose by nearly 26% between March 2020 and March 2024 to over $18,000 per year, or $1,510 per month. Add to this the cost to finance the median-priced single-family home of $2,278 per month, and the total cost of ownership rises to nearly $3,800 per month. As a point of comparison, renting a typical single-family home in March 2024 was $2,236 per month, or 30% less. It is because of this cost differential that so many would-be homebuyers are preferring to rent.

In addition, given that more residents are living in communities with HOAs, they’ll need to budget for monthly fees and special assessments. According to the Foundation for Community Association Research, over 75 million Americans live in one of the 30% of residences governed by an HOA, and that number is expected to grow in the years ahead.

Although the national average monthly fee is $259 and generally covers some of the costs otherwise borne by a homeowner not living in an HOA, living in a poorly run community can mean catastrophically high assessments later. That’s why it’s crucial when buying a home in an HOA to carefully examine all governing documents, meeting minutes as well as the most recent annual budget and reserve study.

Housing Shortage Will Last Through the End of the 2020s

With the estimated pent-up demand for housing ranging up to 4.5 million homes, even if the nation’s builders are willing to produce more supply, it still takes time to find suitable land, skilled labor and materials. While the National Association of Home Builders expects this pent-up demand to be supplied between 2025 and 2030, unless there’s a consistently higher rate of legal immigration above the pandemic years, changing demographics by 2030 will eventually result in lower demand for new housing.

National Housing Market Predictions for 2025-2029

The following is a summary for year-end 2024, 2025 and some predictions for the housing market through 2029. Although a recession is no longer predicted, economic growth is expected to decline from the robust rates of 2.9% in 2023 and 2.8% to 3.0% during the second and third quarters of 2024. However, should the country enter a recession, these predictions would change accordingly.

Home Prices: After remaining nearly flat in 2023 but jumping 4.0% year-over-year through October 2024, home prices are forecast to continue rising moderately as more housing inventory is released but rates remain relatively high. By 2025 through 2029, given the large run-up from 2021 through now, home prices are predicted to rise at a percentage point or so above the rate of inflation, for an estimated increase of about 17% from 2024 levels.

Home Sales: After falling sharply in 2023 and 2024 to the lowest levels in almost 30 years, existing home sales are predicted to slowly increase through 2029. Sales of new homes, which continued to rise in 2024 due to builders’ ability to buy down mortgage rates to boost affordability, will expand on those gains throughout 2029 but continue to be limited by competition for buildable land and skilled labor.

Home Rents: After jumping sharply in 2021 and 2022, home rents continued to rise in 2024 at a more moderate pace, especially in those markets that have seen a huge jump in supply. For 2025, overall rents are predicted to continue rising moderately and the percentage increase may be higher for single-family homes. Given ample new supply of multifamily apartments in recent months, their rents are predicted to flatten out or even fall in the first half of the year before rebounding in the second half.

Source: realestate.usnews.com ~ By: Patrick S. Duffy ~ Image: Canva Pro