Here’s a look at the process of calculating the value of your home and what it means for your home’s sale price.

You know how much you paid for your home, and you likely factor the work you’ve done and the memories you’ve made there into your idea of what it’s worth. But while your home may be your castle, your personal feelings toward the property and even how much you paid for it a few years ago play no part in the value of your home today.

In short, a house’s value is based on the amount the property would likely sell for if it went on the market.

Why Should You Know the Value of Your Home?

You should have a grasp of the value of your home in a variety of situations: if you’re getting ready to sell your house, looking to refinance your mortgage or buying a new homeowners insurance policy, for example.

For a better understanding of what your home’s value means, how it may change over time and what the impact may be if the housing market shifts significantly in your neighborhood, city or even the whole country, here’s our breakdown.

If your property value is based on what a buyer is willing to pay for it, all you have to do is find someone willing to pay as much as you think it’s worth, right?

Determining a home’s value is a bit more complicated. Keep in mind that buyers place no value on the good times you’ve spent there and might not consider your updated bathroom or in-ground swimming pool to be worth the same amount you paid for the upgrades.

And even if you find a buyer willing to pay $450,000 for your home, the value of your house isn’t necessarily $450,000. Ultimately, the financial backing in a deal determines the property’s value, and it’s most often a mortgage lender making the call.

Property valuation primarily takes into account recent sales of comparable properties in the area. Key identifying factors are the same square footage, number of bedrooms and lot size, among other details. Professionals who determine property values for a living compare all the details that make your house similar and different from those recent sales, and then calculate the value.

But when your property is unique – maybe it’s a triangular lot or a four-bedroom house in a neighborhood full of condos – determining the value can be more difficult.

The individual, group or tool appraising the property may also influence the outcome of the appraisal since they all appraise properties differently for a variety of reasons. Here’s a look at common appraisal scenarios.

Lender Appraiser

In the case of a property sale, the appraisal often happens once the property has gone under contract. The lender will hire an appraiser to complete a report on the property, getting all the details on the house and its history, as well as the details of similar real estate deals that have closed in the last six months or so.

If the appraiser comes back with a valuation below that $450,000 sale price you’ve agreed upon, the lender will likely state that it is willing to lend an amount equal to the property’s value as determined by the appraisal, but not more. If the appraisal comes in at $425,000, the buyer has the option to come up with the $25,000 difference or try to negotiate the price down.

Sellers are often open to negotiation at this point, knowing that a low appraisal likely means the house won’t sell for a higher price once it’s back on the market, though excessive interest in a property may be able to sway an appraiser.

Lindsay Katz, a real estate agent with Redfin in the Los Angeles area, says low inventory and high demand has made the Los Angeles market extremely competitive. In cases of multiple offers on a home that drive the price above its initial asking point, a higher value becomes easier to prove to an appraiser that the market value of the home has risen. “I don’t know how you can’t justify that price when 13 people agree,” Katz says.

Appraiser You’ve Hired

If you haven’t yet put your house on the market and are struggling to determine price, hiring an appraiser can help you get a realistic estimate.

Especially if you’re struggling to agree with your real estate agent on what the most likely sale price will be, bringing in a third party could provide additional context. The cost of a formal appraisal is about $350 on average, according to home services company Angi.

Online Home Value Estimator

Many real estate information sites offer more informal home appraisal tools that will give you a ballpark value for your home. You may have previously taken a look at U.S. News’ own home value estimator, Zillow’s Zestimate, realtor.com’s RealEstimate tool or explored the Federal Housing Finance Agency’s House Price Calculator.

It’s important to keep in mind that an online home value estimator is simply pulling from available information online and may not have all the facts that a professional appraiser would utilize in a valuation report. The online algorithms can catch many details, but they don’t necessarily have the ability to account for more localized factors, like the impact of severe storm damage or trends taking place in your city.

“There’s a lot of information out there,” says Danielle Hale, chief economist for realtor.com. “They don’t always agree, depending on how unique your home is or if there aren’t a lot of sales where your home is.”

Your home’s value also determines annual property taxes. In addition to examining the sale prices of similar houses that sold recently, a tax assessor looks at what the cost would be to build a similar house, whether you’ve done any recent improvements, if you earn income from the property and the cost of upkeep.

A property’s assessed value for tax purposes is often less than the appraised value – and that’s a good thing. The property taxes you pay annually are based on the assessed value, so the higher it is, the more you owe.

How Do Market Values Apply to My Home?

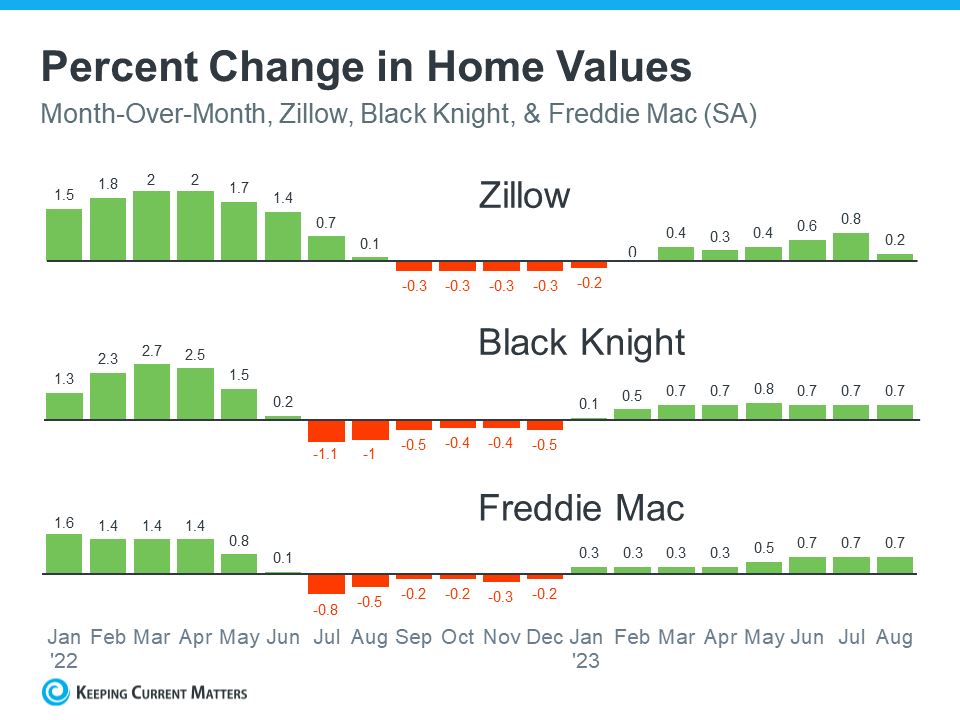

There are multiple ways to find out the current value of your house, but individual appraisals and assessments aren’t the only cases where you’ll hear about home values. In annual, quarterly or even monthly reports, home values are often discussed along with the rising cost of homeownership on a local, state and national level.

Depending on the source of information, reported values may be based on online estimator tools, listing prices for houses currently on the market or property value information from local assessors’ offices. These numbers are useful to discuss trends on a large scale, but they don’t always reflect the actual sale prices of real estate deals that closed in those time periods.

The details you get about rising values can be useful as you prepare to put your home on the market, buy your first house or learn more about economic forecasts, but don’t take national trends as indicators of what’s happening in your area.

The importance of trends in home values depends on the stage of homeownership you’re in or moving toward. Here’s what you should know:

As you’re preparing to start house hunting, keeping up on real estate market trends can be an excellent way to know what you’ll be facing. If values are climbing every month and year-over-year comparisons show fast growth – for example, 5% or more – those are signs that a lot of buyers are looking for houses at the same time as you. In mid-2021, home values were climbing at an incredibly fast pace, and the median sale price in the U.S. was seeing more than 20% year-over-year growth. Don’t expect this to repeat soon.

For Investors

Whether you’re looking to invest in a property for rental income or buy a fixer-upper for a quick turnaround, current market trends may influence your choice of purchase. In Los Angeles and many other parts of the country, more time spent at home during the pandemic caused many buyers to shift their focus when looking for a place to live. Instead of prioritizing proximity to shopping and nightlife, for example, “people renting or living in a condo are thinking they’d like to have a backyard, perhaps a pool,” Katz says.

But before you invest in a sprawling property with all the outdoor amenities, learn more about the market and its previous trends. You’ll also want to crunch the numbers to see if rent will be able to cover the mortgage and upkeep on an income property.

If you’re preparing your home for sale or just looking to learn more about your net worth, keep in mind that wider home value trends and reports have little impact on you.

Instead, keep a close eye on local reports; those that provide monthly or quarterly trends on your specific ZIP code can be a better reflection of what’s happening to your property value, Hale says.

Especially if you’re considering selling your home, a knowledgeable real estate agent could be your best source in understanding your property value. “You would want to reach out and talk to an agent and get a local expert’s assessment,” Hale says.

On the other hand, “if you’re not selling, a (positive) change in value still might help you feel wealthier,” says Hale, noting that a current valuation of your home may help you make future financial decisions.

How Can I Increase My Home’s Value?

Whether you’re planning to sell now or in a couple of years, or you’re simply looking to make your home as valuable as possible in the long term, you can potentially help increase its value with regular maintenance, renovations or even additions that could appeal to homebuyers.

Short Term

Many homeowners are motivated to add value to a property when they’re preparing to sell. It’s not impossible to add a couple of thousand dollars to the price tag with some simple remodeling projects that can make your home look fresh and appeal to buyers. Here are a few:

-

- Fresh paint in neutral colors.

- New landscaping.

- Smart thermostat.

- New or refinished cabinets.

- New or well-maintained roof.

- New or well-maintained furnace or air conditioning.

Maximizing value isn’t just about cosmetic fixes – it’s also about focusing on key areas like the roof and HVAC systems that would come up in a home inspection. Issues like leftover water damage on the ceiling from an old roof leak or a cracked window will show up in the home inspector’s report. If anything concerns the buyer too much, you may run the risk of the deal falling through.

Midterm

If you’re looking to make changes to your home so it’s on par with a different caliber of properties in your neighborhood, consider these larger construction projects:

-

- Primary suite addition.

- Guest bedroom add-on.

- Finished basement.

- Garage construction.

- Complete kitchen renovation.

- Bathroom addition.

These more extensive changes can be an excellent way to take your home to the next level, but only if other houses like this exist in the area. Adding a master suite and new garage to a neighborhood full of two-bedroom bungalows with street parking won’t make the property appraise much higher than the others. That’s because your house may no longer appeal to the typical buyer in that neighborhood.

Long Term

If you’re looking to increase your home’s value for the sake of your overall wealth, the best thing you can do is continue to pay off your mortgage and gain equity in the property. With proper upkeep and work to keep the home up to date, your home value will, on the whole, naturally increase over time.

Source: realestate.usnews.com ~ By Devon Thorsby ~ Image: Canva Pro